Imerys, the world’s leading industrial minerals group, in a significant move for the industrial minerals sector has closed its purchase of Greek industrial minerals group S&B Industrial Minerals SA.

The buy brings considerable mineral assets to the French multinational, in particular bentonite, perlite, and wollastonite.

S&B’s perlite processing plant and port at Voudia, Milos Is., Greece, one of many perlite facilities in Europe, the USA, and China that will augment Imerys’ existing perlite business. Courtesy S&B

The acquisition started in November 2014 and closed Friday 27 February 2015. The price was determined on the basis of an equity value of €525m for all shares, increased by a performance amount not to exceed €33m.

It was paid in cash for approximately €311m, financed by a bond issue completed by Imerys in December 2014, and by the issue of 3.7m Imerys shares on a pre-emptive basis to the Kyriacopoulos family, S&B’s shareholder for more than 80 years.

The Kyriacopoulos family now has an approximate 4.7% interest in Imerys, and has entered into a shareholders’ agreement with Imerys’ majority shareholder since 2011 (currently at 56.2%) Groupe Bruxelles Lambert (GBL). GBL is the second largest holding company in Europe, and also has interests in Lafarge (21.0%), SGS (15.0%), and Umicore (5.6%).

S&B’s former CEO, Kriton Anavlavis has now joined Imerys’ Executive Committee as Chief Financial Officer (CFO), replacing Michel Delville who held the position since 2009.

Anavlavis, a graduate of Newcastle University, UK and INSEAD, joined S&B in 1990. He was manager of the Bentonite Division from 1995-2007, became CFO from 2008-2011, then CEO from April 2011.

Imerys gains from S&B

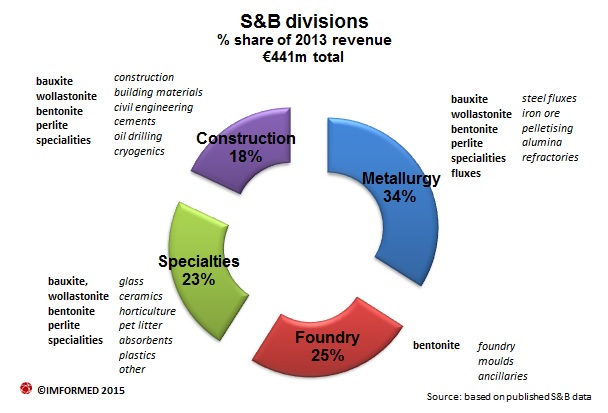

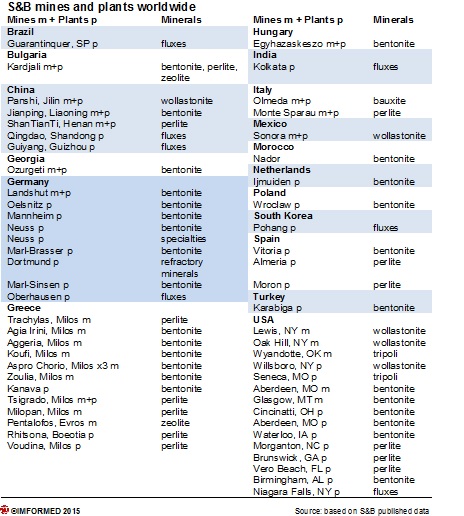

With the S&B purchase comes a considerable clutch of mineral assets totalling some 31 mines, 51 plants, and 28 distribution centres across 22 countries – as well as 1,838 employees (see accompanying charts).

The key gains for Imerys, aside from extensive global sales and distribution centres, are synergies in bentonite and perlite, and new arrivals (for Imerys) in wollastonite and metallurgical fluxes.

The bentonite gain neatly fills a much needed gap in Imerys’ oilfield minerals division, especially since Imerys lost out to Minerals Technologies Inc. in bidding for US bentonite leader Amcol during 2014 – indeed, perhaps that was the spark to focus on S&B to begin with. CEBO International also gives Imerys access to the North Sea oilfields.

Significantly, S&B’s bentonite brings mines and plants not only in Europe, but also in the USA and China. It also dovetails nicely with Imerys’ existing foundry minerals supply, and the white bentonite from Morocco supplies the higher value filler markets.

The other key synergy is perlite, also spread across the USA, Europe, and China. The USA is neatly tied up now with Imerys’ existing facilities (formerly World Minerals) covering the western USA, and S&B’s facilities covering the eastern USA.

Interestingly for Imerys, S&B’s bentonite and perlite activities also open up central and eastern European opportunities in Hungary, Bulgaria, and Georgia.

Imerys can now add wollastonite to its extended portfolio, since in just 2012, S&B acquired world leader NYCO Minerals Inc., USA. This interesting mineral has key markets in ceramics, plastics, paints, and metallurgical fluxes – all served by Imerys – but has its main sources limited to single producers in the USA (Imerys), China, India, and Mexico (Imerys) – so the wollastonite supply market is pretty much cornered.

Metallurgical fluxes are also a new(-ish) addition to Imerys. No doubt the group’s bauxite and carbonate experts, if not active in, will be already familiar with this market application, but the addition of S&B’s world leader Stollberg brings this large volume market for industrial minerals into the spotlight.

Fluxes are vital to the steelmaking process and wollastonite finds use in continuous casting fluxes. Other mineral fluxes and conditioners include lime/dolime, olivine, fluorspar, bauxite, and magnesite.

Beyond these main gains, Imerys will also now be aware of a range of other imported minerals that were handled by S&B through its German processing plants (ex-Otavi Minen AG) including: barium carbonate, brown fused alumina, calcined bauxite, chamottes, and mullite.

Another interesting gain for Imerys is the Sardinian bauxite resource operated by Sardabauxiti SpA, the last remnant of S&B’s once large bauxite business.

During the mid-late 2000s, S&B had been having various problems with its Greek bauxite operations, causing concern to its non-metallurgical bauxite customers, such as calcium aluminate cement producer, Kerneos SA (reacting by seeking other sources). In November 2011 a process was set in motion to gradually divest the Greek bauxite operations to Aluminium SA, Greece. However, after due diligence, the deal foundered in October 2012.

Then, on 20 February 2015, the Greek bauxite operations of S&B, now parcelled as European Bauxites, were sold to Kerneos SA and Greek bauxite producer ELMIN (in 2012 Kerneos bought a 54% stake in ELMIN).

When the Imerys acquisition of S&B was first announced in November 2014, it was stated that “European activities of bauxite production for metallurgy would be excluded from the proposed transaction perimeter.” Presumably, the intention was always to divest the Greek bauxite and perhaps Kerneos/Elmin were already waiting in the wings.

Left out of the deal apparently was the 300,000 tpa capacity underground bauxite mine and plant operated by Sardabauxiti, at Olmeda, Sardinia, Italy. S&B restarted the mine in 2004, eventually acquiring Sardabauxiti in 2007.

The Sardinian material is boehmitic, with a lower iron content than the Greek diasporic bauxite. In the past, metallurgical markets have accounted for about 60% of output; non-metallurgical markets include cement, calcium aluminate cement, and mineral wool manufacture.

How Sardabauxiti will be integrated into the Imerys group remains to be seen, but with the recent interest and investment in ceramic proppant manufacture, Imerys may well evaluate this resource as a possible ceramic proppant feedstock raw material should demand take off from shale gas development in Europe, but more likely in the Middle East and North Africa.

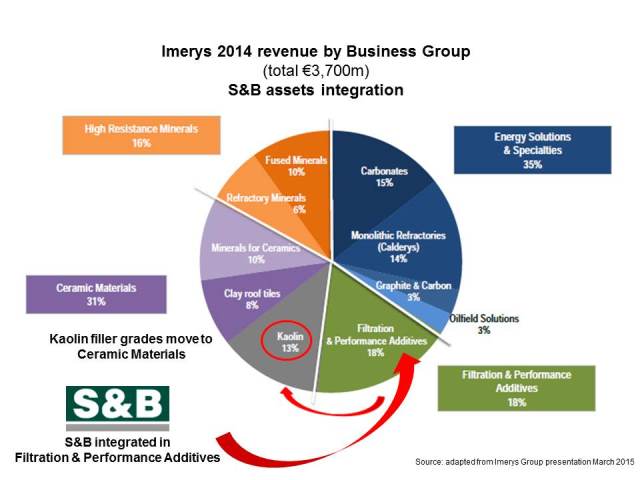

It’s a possibility that the initial home of S&B in Imerys’ Filtration & Performance Additives Business Group might be temporary, or at least the division title may be modified. With its metallurgical flux component perhaps there may be some way that minerals used in high temperature applications (often associated with metal manufacture) might come back together again in a refractories-foundry-fluxes group. We shall see.

Mineral Recycling Forum 2016, 14-15 March 2016, Rotterdam

Learn about the fastest evolving sector of the industry: Secondary Raw Materials supply chain and marketsMineral Logistics Forum 2016, 11-13 April 2016, Rotterdam

The networking and knowledge hub for industrial minerals logistics from mine to market

Fitting it all together

At present, Imerys has said that S&B’s assets will be lodged with the current Filtration & Performance Additives Business Group.

One of the key ramifications of Imerys’ seemingly unstinting mission to acquire most of the world’s leading industrial mineral producers is that each time a major acquisition occurs – say every 2-3 years – it means that a major restructuring of the group’s business divisions is likely to take place soon after in order to accommodate the new assets in an intelligent as possible manner.

However, as Imerys knows well by now, the versatile market application nature of most industrial minerals means that they serve more than one market sector, and in fact a single mineral frequently supplies five or more markets.

This can makes things a little frustrating when attempting to snugly fit new mineral operating assets into an existing business division structure based on end user sectors.

This has indeed been Imerys’ rationale since it made the decision (then as Imetal) to cross the Rubicon from metals to non-metals in 1990. And it makes sense, until you start adding more minerals and producers and then the market cross-over factor starts to go into overdrive.

This is not to suggest that Imerys’ growth model has no focus. Far from it, the Imerys model is clearly to acquire leaders in their field and generally in line with their existing market strengths.

So for example, core Imerys strengths include refractory minerals for acidic refractories (eg. bauxite, mullite, andalusite), minerals for functional filler markets in paper, paint, and plastics (eg. calcium carbonate, kaolin, talc, mica), and fused minerals for refractories and abrasives (fused aluminas, fused zirconia). Big name acquisitions over the last two decades have broadly followed such market divisions.

It simply demonstrates the market versatility of industrial minerals that even with such a model, you are going to get market cross-over. Indeed, it underlines what should always be the industrial mineral producer’s mantra – “Diversification, Diversification, Diversification”. Never have all your mineral product eggs in one market basket!

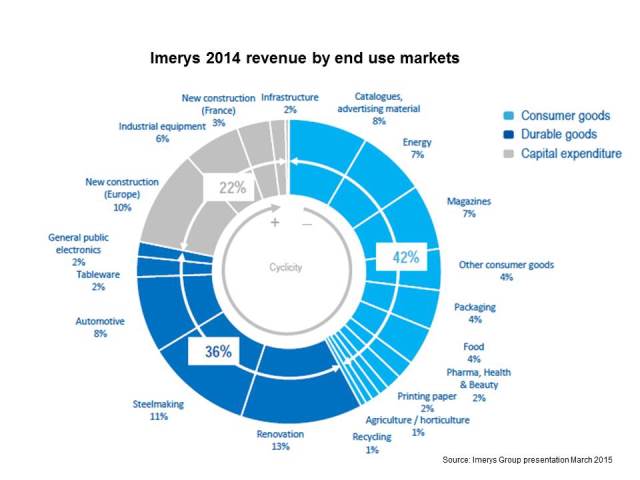

Take a look at the accompanying chart showing the current spread of Imerys’ end use market sectors. A very wide range of markets each using several same minerals as raw materials.

However, when seeking to grow into new markets, then the existing structure needs to be modified. In the past, Imerys had divisions entitled Paper Pigments for example. So when certain acquisitions came along which clearly did not fit anywhere, such as perlite and diatomite with the World Minerals buy in 2005, then “…and Filtration” would get tagged on to the chosen recipient division, in that case “Performance Minerals & Filtration” was formed.

Another example is when Imerys acquired Luzenac Talc from Rio Tinto Minerals in 2011 (the latest major buy before S&B). There are clearly significant markets for talc in both the ceramics and in the higher value functional filler (“Performance”) sectors – so talc has been spread across the group, so to speak.

Interestingly, Imerys’ recently formed Oilfield Solutions division has almost materialised on its own accord. Sure, Imerys started investing heavily in ceramic proppants in 2011 to catch the “shale gale” storming across North America. But through acquisitions and growth over the years Imerys has had for some time a wide portfolio of oilfield minerals sprinkled across its stable, they just needed to be tied together, and the push for proppants was the catalyst (although market conditions have recently dipped owing to the oil price crash and have led to temporary closures of the new ceramic proppant plants).

Thus, as the group has evolved, Imerys has switched to using terms such as “Specialties”, “Additives”, “Performance”, “Energy”, and “Solutions” for its division titles in order to accommodate its swelling mineral portfolio but at the same time avoiding having to somehow indicate each market being served.

The problem with this approach of course, is that the business division starts to lose its face value identity. For example, which minerals are represented in “Performance Additives” of the “Filtration & Performance Additives” Business Group? Actually, it’s “mainly talc and mica”, but this is not obvious unless one does some digging. And Ceramic Materials now includes the high value functional filler markets for kaolin.

But it would be tortuous to have to indicate each mineral in the name of each division, so market groupings are probably the best way to go here, and just accept the fact that there will be some divisional mineral overlap.

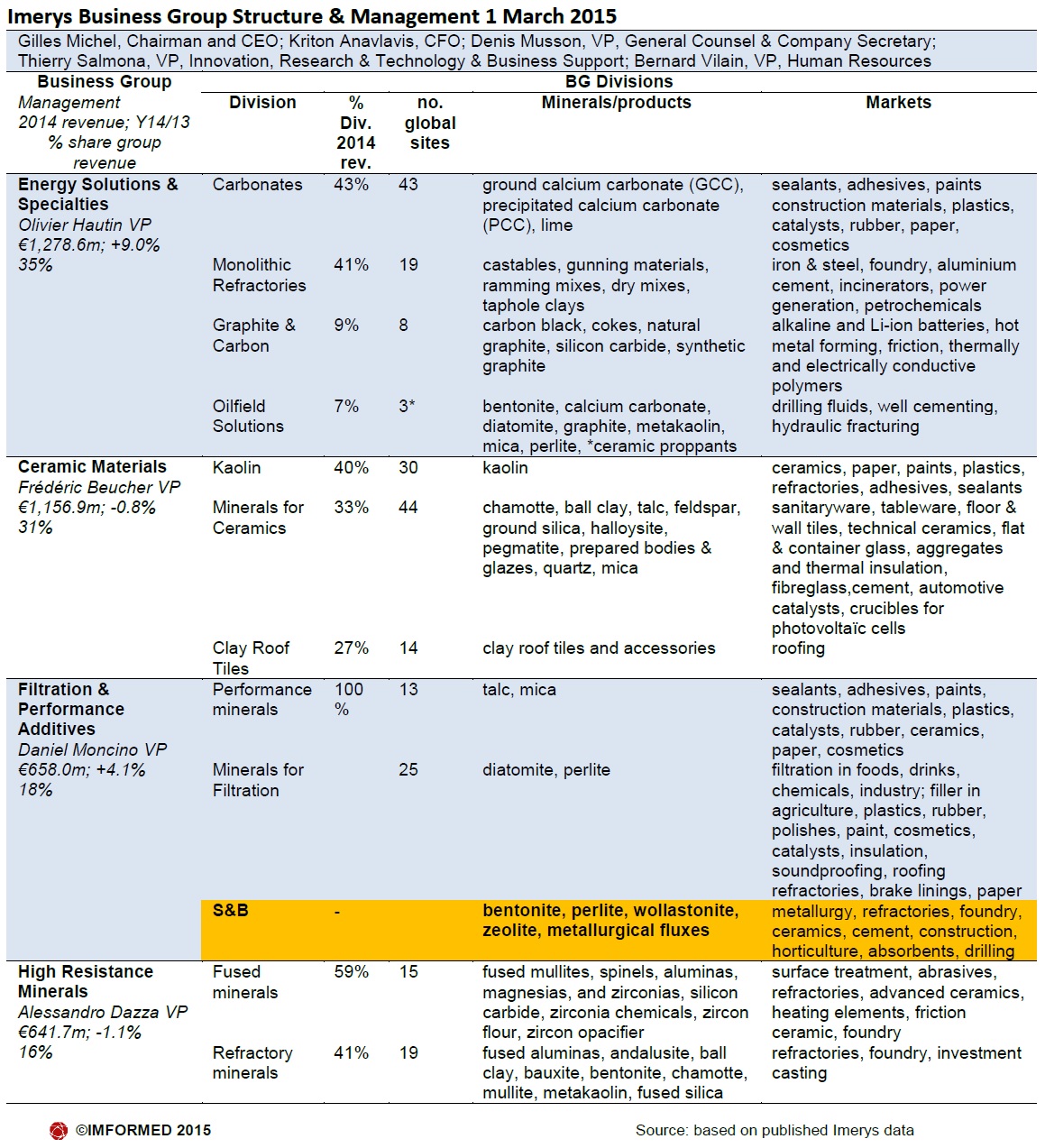

See the accompany chart for the latest Imerys structure with its split shares of total group revenue. Then see the accompanying table showing the Business Groups in more detail, in particular noting the respective minerals and markets, and where S&B’s minerals assets are destined.

Defining decade: the 90s’ pursuit of industrial minerals

There are similarities between these two companies. Both Imerys and S&B have history steeped in mining and processing natural resources, and in the last two decades each have been extremely acquisitive and have grown significantly, including raw material ventures in China.

Established in 1880, as Société Penarroya—Le Nickel (SLN), Imerys’ original activity was mining and transforming nickel. The core business remained the extraction and processing of non-ferrous metals for almost a century. The 1970s were the first milestone when the group’s companies were brought together and diversified under the name Imetal.

Then in the 1990s, Imetal clearly signalled its future strategy by doubling in size and making a series of significant US and European acquisitions in the industrial minerals sector in clays, calcium carbonates, refractory minerals, ceramics, and graphite.

The second milestone in 1999 saw Imetal acquire UK minerals giant English China Clays (ECC; kaolin, carbonates), divest its Metals Processing business, and change its name to Imerys. Since then the group has continued on its acquisition trail, with S&B being the latest target, and perhaps the most mineral-diverse since ECC.

S&B started life in 1934, founded on Milos island, Greece, as Silver & Baryte Ores Mining Co. SA, mining and exporting barytes, together with Bauxites Parnasse Mining Co. SA in Fokis, Greece, mining and exporting bauxite.

During the 1950s, S&B added bentonite and perlite to its Greek minerals portfolio. While the mineral businesses were strengthened over the years, it was not until the early 1990s – like Imerys – that S&B really started to acquire and grow considerably.

That busy decade saw Bauxites Parnasse absorbed into S&B, a listing on the Athens Stock Exchange, the founding of IKO-Erbslöh GmbH (bentonite), acquisitions of Sarda Perlite Srl, Otavi Minen AG (processing), Mykobar Mining Co. SA (bentonite, perlite, Greece), Askana Ltd (bentonite, Georgia), and start-up of a perlite plant in China.

The 2000s were equally active with a name change to S&B Industrial Minerals SA in 2003, acquisitions of Bentonit Hungaria Kft, Sardabauxiti SpA , Bentonit AD (Bulgaria), ΝΑΙΜΕΧ S.A.R.L. (white bentonite, Morocco), Stollberg Group (Germany, metallurgical fluxes), CEBO International BV (50% Halliburton; oilfield mineral distributor), bentonite plants in the USA and Germany, and starting bentonite and perlite operations in Turkey, and in wollastonite in China (Orykton GmbH, a j-v with Quarzwerke GmbH).

In 2012, S&B acquired world wollastonite leader NYCO Minerals Inc. The following year S&B delisted from the Athens Stock Exchange as the private equity group Rhône Capital invested in S&B, and S&B Minerals Finance SCA was established in Luxembourg as the new parent entity of the S&B Group. A bentonite joint venture was established in China.

Future targets

With Imerys it’s possible that anything is up for grabs. But taking into account the group’s existing market interests, there are a few options for discussion:

Oilfield: the glaring absentees here are silica sand (frac sand) and barytes. The market is North America for frac sand, and the supply sector is well buttoned up with established major players. Outside China and India, the main barytes producers are captive to leading oilfield service groups and it is unlikely that they will relinquish their secure barytes sources.

Refractories: always a talking point about the anomaly of hosting a monolithics business, ie. a mineral user, whereas all the other businesses are mineral suppliers, and whether Imerys will divest this at some stage to the much consolidated refractory market. Another question is whether Imerys will move into supplying refractory minerals for basic refractories, eg. mag-carbon bricks, and look for magnesia and (more) graphite sources.

Glass/ceramics: Rio Tinto may yet make another attempt to sell its considerable borates business, which includes a soda ash source and lithium prospect. That might come down to a fight between Imerys and Sibelco.

Batteries: already possessing graphite sources, other battery raw materials might be attractive, such as lithium. It might be that Imerys, along with others, is biding its time to see just how and when the lithium battery revolution really kicks off.

With such a massive merger, the S&B integration will take some time to settle in, and with the world economy looking to right itself again, it may be assumed that Imerys’ appetite for acquisitions has been sated for now and a “quiet period” may ensue for the time being. But, you never know…

Once again a great article. Meaningful.

I have been in contact with S&B since the early 90s in regard to their perlite logistics. Lots of fine memories of their former HQ at Amerikis Street. Today’s reality makes me wonder what the impact of this takeover will mean, logistically speaking, for current S&B business via Rotterdam and Amsterdam ?? There is a very nice Imerys terminal in Antwerp which is fully booked today….???

Great article Mike. There are a number of further rationalizations possible in the IM sector, particularly in lime, alumina and to a lesser extent in magnesia products and now is a good time with the low cost of borrowings. It will also be interesting to see how the major IM companies approach the next (but longer term) potential growth areas in Afric and India.