With rising recognition of fluorspar’s “criticality” in its derivatives’ use in lithium-ion batteries and semiconductors, not to mention mainstay applications in fluorochemicals, steel, aluminium, and ceramics, the mineral is receiving increasing attention (see presentations review below).

In particular, there is much activity from new players attempting to develop new and alternative sources of fluorspar, assess exciting growth markets, as well as leading consumers evaluating where to source fluorspar outside China.

Title Image Blue Sky Thinking For Fluorspar: the primary fluorine-bearing mineral has a wide range of uses, from cement (main image: one of Tamer Mining’s cement grade fluorspar mines in central Turkey) to microchips (inset top left); there is growing interest in recycling fluorine from waste streams, such as phosphate rock processing waste (inset top middle: phosphate rock waste at OCP, Morocco, is to be processed in a new plant underway by Fluoralpha); (inset top right) delegates enjoying networking on Lake Maggiore at Fluorine Forum 2025 – to which we shall return for Fluorine Forum 2026, Baveno, 26-28 October. Images courtesy: Tamer Mining, F2ChemTech, Fluoralpha

All these trends and developments are scrutinised and discussed at IMFORMED’s annual Fluorine Forum – the premier event for the international fluorine raw materials and markets business.

Last year Fluorine Forum 2025 was held at the Grand Hotel Dino at Baveno, Lake Maggiore, Italy. And what an event it was!

Whether learning about increased Chinese fluorspar capacity, FSA developments in Morocco and Italy, latest LiPF6 and semiconductor market trends – there was something for everyone in this spectacular setting with a record attendance of over 200 attendees.

The panel of expert speakers covered a range of topics:

SUPPLY/DEMAND OVERVIEW | CHINA | ITALY | MEXICO | FSA | HF | ALF3 | FLUOROCHEMICALS | BATTERIES | SEMICONDUCTORS | CEMENT | NUCLEAR

For a full review of Fluorine Forum 2025 presentations please see below

The well-attended and most convivial Welcome Reception, sponsored by Fluorsid, was just a few minutes boat ride across to Ristorante Italia, on the wonderful Isola Pescatori, one of the famous Borromean Islands on Lake Maggiore.

Always the most professional event for all the players in the market with the latest news and market movements.

Xu Yue, General Manager, Shanghai Zhengkaiyuan Industrial Co. Ltd, China

Thank you again for organising such a wonderful conference. The venue was spectacular, and strong attendance made for very robust business discussions, which has become a cornerstone of your events.

Jim Juron, Traxys North America, USA

Excellent. Interesting and accessible location. Well run and good conference room, and lots of places to meet.

Mark Cooksey, Managing Director and CEO, ABx Group Ltd, Australia

Thank you for the wonderful organisation of Fluorine Forum 2025. It was an exceptional event!

Dr Bob Syvret, Principal/Owner, Fluorine Chemistry and Technology LLC, USA

“In this changing world, with events happening faster and faster and meetings more and more often held across a screen, I believe it is very important that industry players have first-hand knowledge of each other — perhaps over a glass of wine or a good Italian espresso.”

President Tommaso Giulini, welcoming the delegates to Fluorine Forum 2025.

This year we are returning to the superbly located Grand Hotel Dino in Baveno, on Lake Maggiore, for Fluorine Forum 2026, 26-28 October. We already have an exciting confirmed speaker line-up (see below), and have attractive Early Bird Rates for a limited period – BOOK NOW!

CONFIRMED SPEAKERS

PFAS latest developments & what it means for the EU fluoroproducts market

Patricia Muñoz, Sector Manager, FluoroProducts & PFAS for Europe (FPP4EU), & Angelica Candido, Sector Manager, European Fluorocarbons Technical Committee (EFCTC), CEFIC, Belgium

Shipping market impact on fluorspar freight

Robert van Muiden, Managing Director, Rotterdam Bulk Logistics (RoBuLog), Netherlands

Navigating sulphur & sulphuric acid markets through geopolitical shifts

Freda Gordon, Director, Acuity Commodities, UK

From waste streams to fluorine supply: Financing global projects

Nicholaus Rohleder, Co-CEO, Fluorcycle & Aaron Ratner, Partner, The New Industrial Corp., USA

Overview of Mongolia’s re-evaluated fluorspar reserves & policy and legal framework supporting foreign investment

Tsevegmed Sandiv, Vice President, Mongolian Association of Fluorite Miners, Manufacturers & Exporters, Mongolia

Redevelopment of fluorspar mining in Northern Europe (UK & Germany)

Peter Robinson, Managing Director, Fluorspar Ventures Ltd, UK & Konstantin Deichsel, Manager Business Development, Deutsche Flussspat GmbH, Germany

Hicks Dome: an unconventional fluorspar deposit for future critical minerals markets

Laurence M. Nuelle, Vice President of Critical Minerals Development, Hicks Dome, LLC, USA

Illinois-Kentucky Fluorspar Project: background, status & objectives

John Lee, CEO, CleanTech Vanadium Mining Corp., Canada

South Africa’s role in enhancing security of supply: New fluorochemicals and fluorspar capacity

Ivan Radebe, Director, Fluorchemicals South Africa Pty Ltd, South Africa

Hydrofluoric acid overview & outlook for fluorochemicals

Samantha Wietlisbach, Global Lead – Inorganics and Minerals Research and Analysis, S&P Global, Switzerland

The aluminium market & demand for aluminium fluoride

Lungile Skhosana, Senior Critical Materials Research Analyst, Project Blue, South Africa

Fluorspar use & demand in Li-ion batteries

Ciara Rice, Battery Chemicals Market Analyst, Benchmark Mineral Intelligence, UK

Developments in HF chemistry and usage in battery, life science, refrigerants and plastics

Dr Max Braun, General Manager, FluorInnovation LLCFZ, UAE

FLUORINE FORUM 2025 REVIEW

INTRODUCTION & OVERVIEWS

Setting the scene: supply spotlight

Mike O’Driscoll, Director, IMFORMED, UK

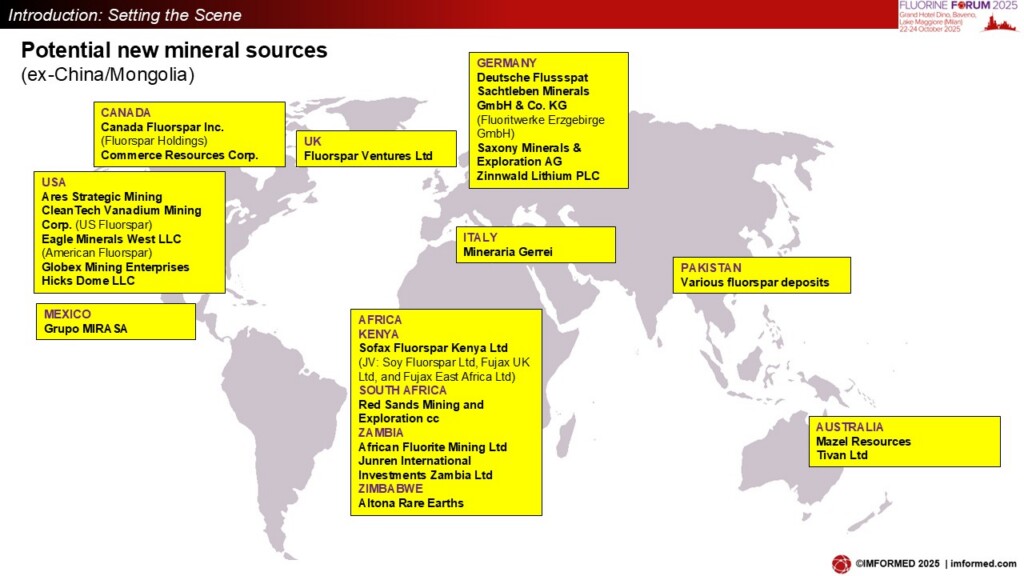

O’Driscoll started proceedings with an acknowledgement of the rising recognition of fluorspar’s “criticality”, followed by a review of potential new sources of fluorspar across the world (excepting China and Mongolia), and some alternative sources of fluorine (mainly recycling from aluminium smelter, phosphate rock, and uranium processing waste).

The projects reviewed fall into one or more broad categories:

- Undeveloped fluorspar deposits

- Undeveloped primary metallic mineral target deposits which have fluorspar as potential by-/co-product, ie. a polymetallic deposit (eg. tin, tungsten, REE, vanadium, lithium).

- New development in historic fluorspar mining district

- Revival of former operating mine

As to which will come to fruition first, there are many influencing factors, such as:

- Financing

- Partnerships

- Legal permitting

- Geology

- Exploration & evaluation programmes to secure resource/reserve estimates

- Mine and plant planning

- Logistics

- Local infrastructure & resources

- Demand for associated primary target (eg. Sn, Li, W, REE, V)

- A feasible consuming market/overall market situation

And if pressed, on a “thumbnail” basis, they could line up as follows:

- Head of the pack “revival” projects: Canada Fluorspar and Sachtleben Minerals GmbH & Co. KG

- Race over next 2-3 years between Mineraria Gerrei Srl, Italy and Ares Strategic Mining, USA

- Others have longer lead times: eg. much rehabilitation work is required for mine revivals of Deutsche Flussspat, Germany and Sofax Fluorspar, Kenya

- Undeveloped deposit projects require more exploration and evaluation, plus mining licences in some cases. Leading this could be Tivan’s Speewah Fluorite Project in Australia.

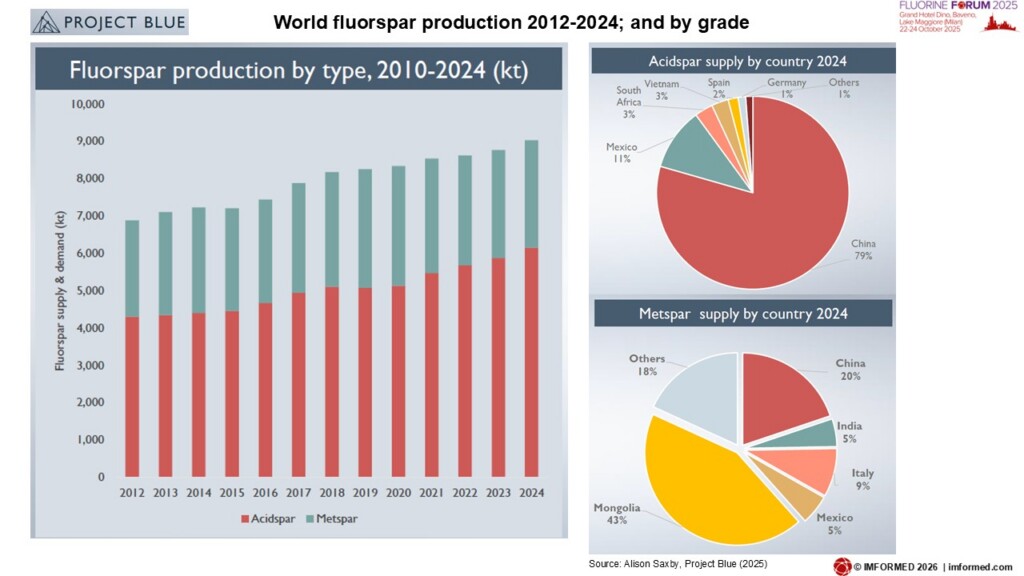

Fluorspar supply & demand outlook

Alison Saxby, Research Director, Project Blue, UK

This presentation covered fluorspar supply, acidspar and metspar, trade, costs of production, fluorspar demand, HF supply, and outlook.

Saxby commented that geopolitics is leading to volatility in many mineral supply chains, and wondered whether fluorspar could be next, before concluding as key takeaways:

Fluorspar supply:

- Acidspar supply is still growing – reaching over 6m tonnes in 2024

- New and historic supply has been bought on-line in 2024 and 2025

- China still dominates acidspar supply, but exports are on a downward trend

- Record exports from Mongolia in 2024

- Additional production in China from by-product material and new mines

Fluorspar demand:

- Fluorspar is crucial to many of the energy transition sectors, as well as traditional markets

- Demand is growing in the lithium-ion battery space, but there could be more modest levels of growth in graphite processing for anode materials.

SUPPLY DEVELOPMENTS: CHINA | ITALY | MEXICO

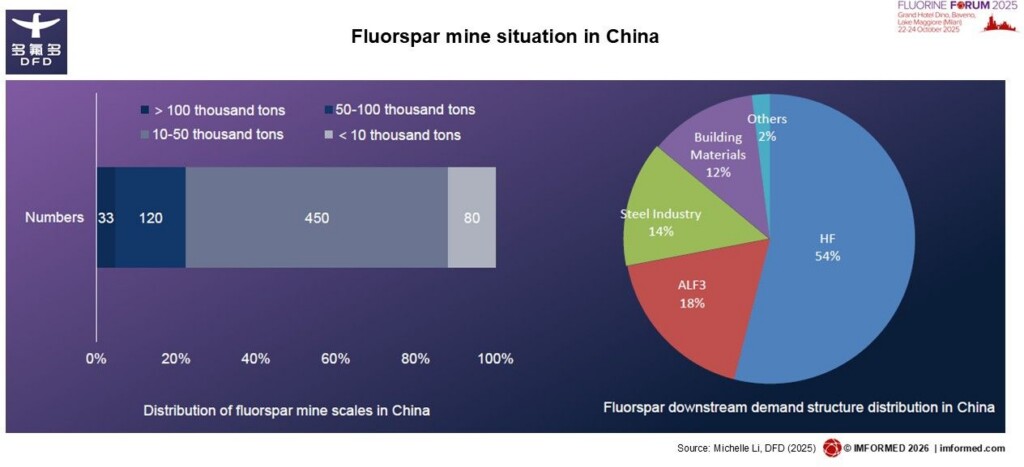

Development trends in Chinese fluorine resource utilisation

Michelle Li, Vice Chairman, Do-Fluoride New Materials Co. Ltd, China

Li placed Chinese fluorspar production in the context of world fluorspar supply, with China’s fluorspar output accounting for over 60% of global production.

Fluorspar production in China is highly dispersed, leading to low industry concentration and a low reserve-to-production ratio.

Chinese fluorspar producers mainly focus on acidspar powder, with chemical industry accounting for about 75% of total demand.

China shifted from being a net exporter to a net importer of fluorspar in 2018, with imports mainly consisting of ~50% grade lump ore <97% CaF2, while exports are primarily 95-97% CaF2 grade.

The growth in China’s acidspar demand is mainly driven by refrigerants, LiPF6, and electronic-grade HF. Demand for AlF3 and other fluorine products remains relatively stable, while HF exports are expected to show a downward trend.

Li pointed out that a large amount of fluorosilicic acid (FSA) remains unutilised in China. Approximately 850,000 tpa of FSA is generated, which could potentially yield approximately 500,000 tpa AHF production.

While China experienced an overall supply deficit of acid grade fluorspar powder from 2023 to 2025, Li forecast that the supply-demand structure for fluorspar powder in China will shift in 2026H2. This will in part be down to new Chinese fluorspar production capacity coming on stream, some 900,000 tpa acidspar capacity is expected from two projects in Xingyang Province.

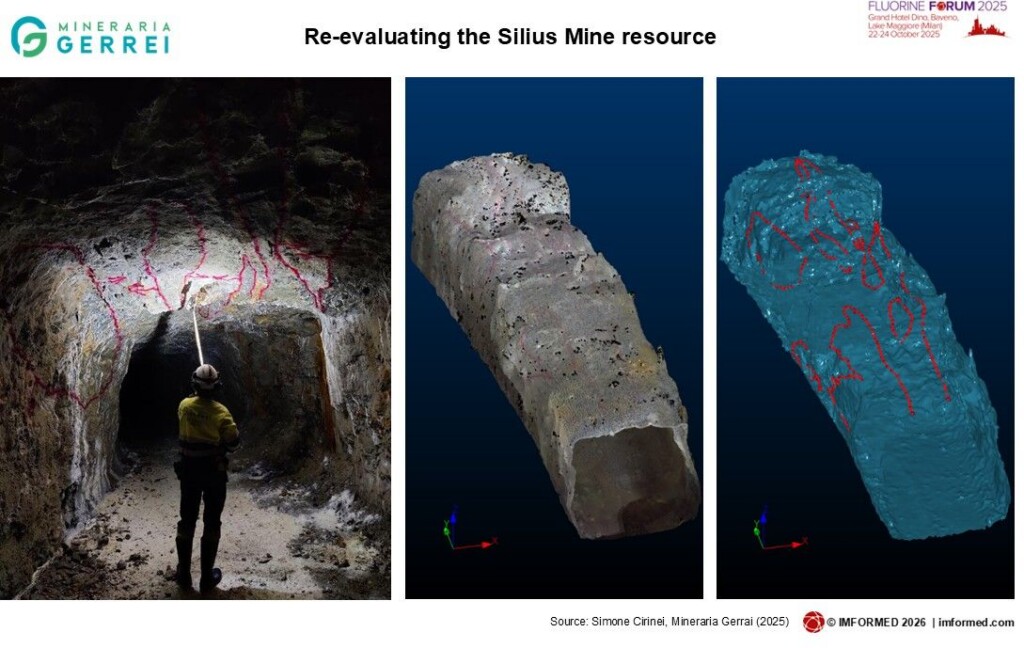

Unlocking Silius’ geological potential: reserves upgrading of Europe’s largest fluorite deposit

Simone Cirinei, Mining Geologist, Mineraria Gerrei, Italy

Founded in 2018, Mineraria Gerrei is reopening and re-evaluating the former Silius fluorspar mine in southern Sardinia.

Silius hosts a world-class fluorite-baryte-galena deposit (4km strike, 600m dip); a narrow-vein system hosted in Palaeozoic metamorphic rocks of hydrothermal origin, comprising 2.2m tonnes of certified reserves with 34.5% CaF2 and 3.2% Pb. The deposit was exploited underground from 1952 to 2007 producing >11m tonnes.

The company has completed a new shaft, is constructing the processing plant and acquiring a fleet of heavy equipment.

The presentation focused on a new geological investigation required to:

- Optimise the extraction: creating models to maximise mineral recovery and minimise host-rock dilution.

- Expand reserves: guiding the choice of sampling locations in accessible non-reserves (>1m tonnes), drilling plans for deeper reserves, and exploration strategies for reserves beyond the lateral boundaries of the deposit.

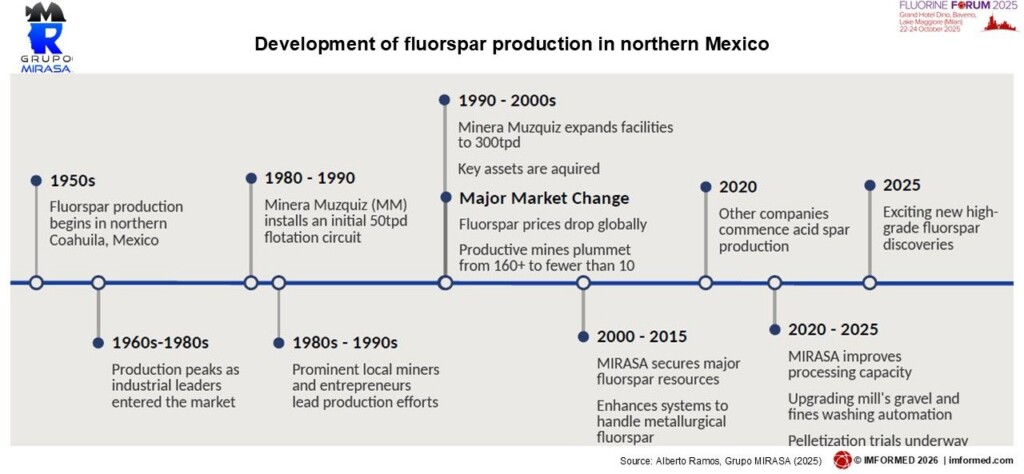

Fluorspar’s future: Northern Mexico’s untapped deposits

Alberto Ramos, Operations Managing Director, Grupo MIRASA, Mexico

Ramos’ paper was an introduction to the untapped fluorspar deposits of the Coahuila region of Mexico and the activity of Grupo MIRASA.

Grupo MIRASA is a growing fluorspar provider in northern Mexico, with a 200 tpd milling plant, Primarily engaged in fluorspar, with additional activities in coal, barite and other steelmaking minerals.

Ramos reviewed the legacy of Ernesto Ground Clayton, a trained metallurgical engineer and geologist from Oklahoma, USA, who in 1942 entered Mexico to locate mercury, manganese, and fluorite deposits for the US during the Second World War.

He laid the groundwork for the first development of Mexico’s fluorspar production centre in Coahuila, now well established.

There are more than 150 fluorspar prospects in the region, some of which were described, with the primary challenges outlined and an environmental plan for future development.

ALTERNATIVE SUPPLY DEVELOPMENTS: FSA | HF | ALF3

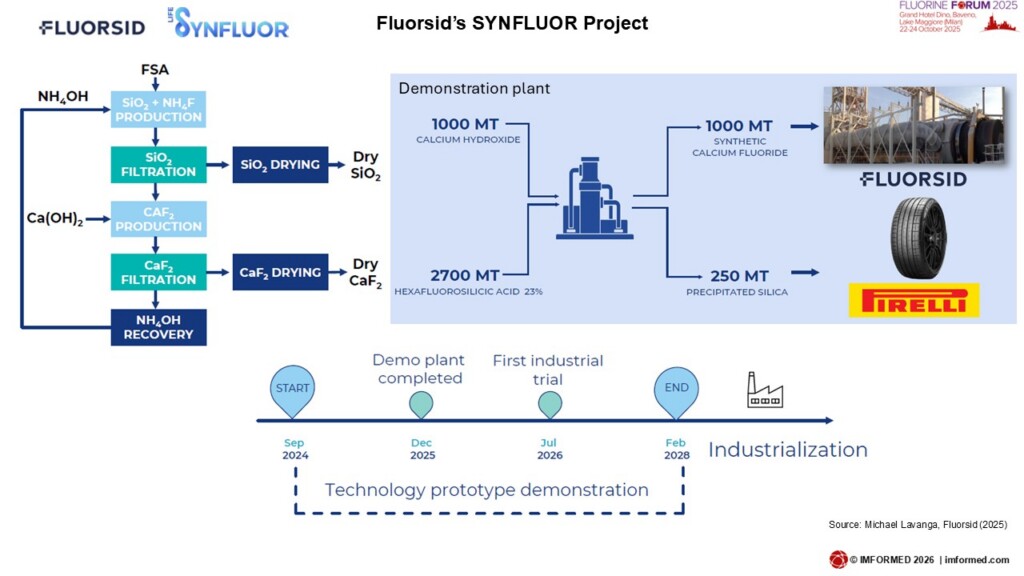

Life Synfluor: circular economy applied to fluorine chemistry

Michele Lavanga, Special Projects Director, Fluorsid, Italy

Lavanga examined the process of turning fluorosilicic acid (FSA) from hazardous waste to a valuable resource yielding synthetic calcium fluoride and precipitated silica, before introducing Fluorsid’s LIFE SYNFLUOR project (co-funded by the European Union, under the “LIFE” programme).

Fluorsid has developed and patented a proprietary technology to convert FSA into high-purity synthetic calcium fluoride and precipitated silica. The former to be used as a raw material for fluorochemicals, thus replacing “natural” acid-grade fluorspar, while the latter to find its main application as a filler in the rubber industry.

Fluorsid is building a demonstration plant at its industrial site in Cagliari, to produce enough fluorspar to feed its industrial fluoride plants for industrial-scale testing. Some of the silica produced will be tested in tyre manufacturing.

Initial industrial trials are planned for mid-2026, and commercialisation from 2028.

The company has established a collaboration with the major tyre manufacturer (and large consumer of silica) Pirelli and with the University of Milano Bicocca, which has great experience and know-how on the properties of silica. Tests on precipitated silica produced in the pilot plant showed similar behaviour to standard commercial silica.

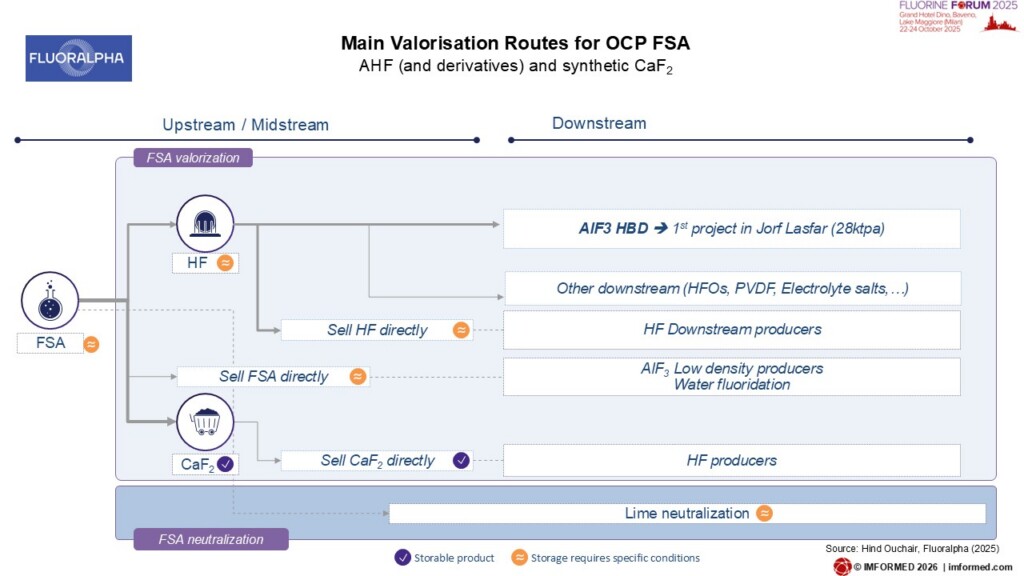

Production of fluorine from Morocco’s phosphate rock

Hind Ouchair, Business Development Director, Fluoralpha, Morocco

Ouchair outlined the fluorine distribution within Moroccan phosphate ore processing (by OCP Group, state-owned world’s largest producer of phosphate rock), before introducing Fluoralpha, established in 2023 to transform the raw potential of Morocco’s phosphate rock-derived fluorine into a range of high-value chemical derivatives.

There are two main valorisation routes for the waste FSA: AHF (and its derivatives) and synthetic CaF2.

A pilot plant is operational and generating samples for testing, while the first industrial plant is under construction.

The first AHF and AlF3 project, 28,000 tpa at Jorf Lasfar, will mobilise less than 10% of total FSA produced by OCP, and is expected on-stream by 2028-29.

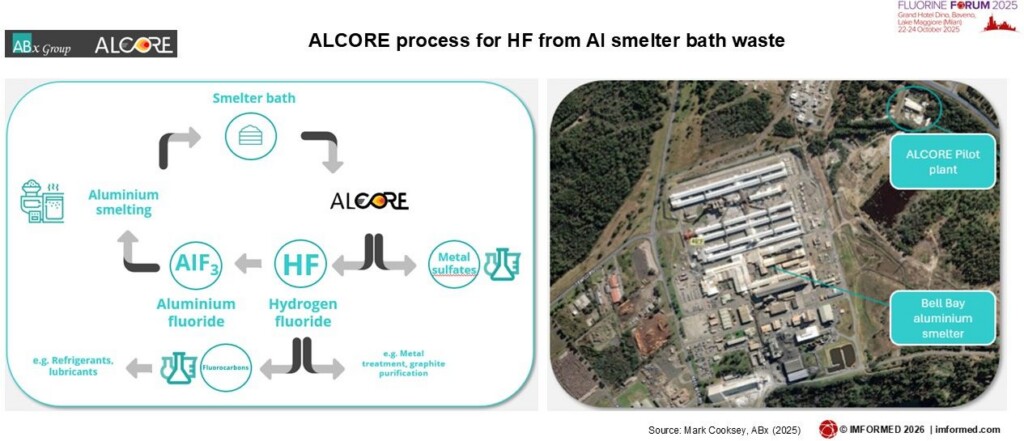

Clean fluorine chemical production: producing industrial chemicals from aluminium smelter by-product

Dr Mark Cooksey, Managing Director & CEO, ABx Group Ltd, Australia

Cooksey introduced ABx Group, and in particular its ALCORE division, which is developing production of industrial chemicals (HF and AlF3) from aluminium smelter by-product.

The aluminium smelting process was explained, revealing two main fluorine-bearing waste flows as a result of AlF3 addition during the process: waste refractories and waste aluminium smelter bath.

ALCORE is aiming at producing low-cost hydrogen fluoride production using aluminium smelter bath by-product, enabling hydrogen fluoride production in Australia, and reducing 100% reliance on imports.

From its batch pilot reactor, ALCORE has processed 4kg crushed bath and 6kg H2SO4 from which 97% of fluorine was extracted from the bath as HF in a two stage process.

The plan is to construct a continuous pilot plant near to Rio Tinto’s Bell Bay aluminium smelter in Tasmania during late 2025-2026, with a view to starting a commercial plant in 2027.

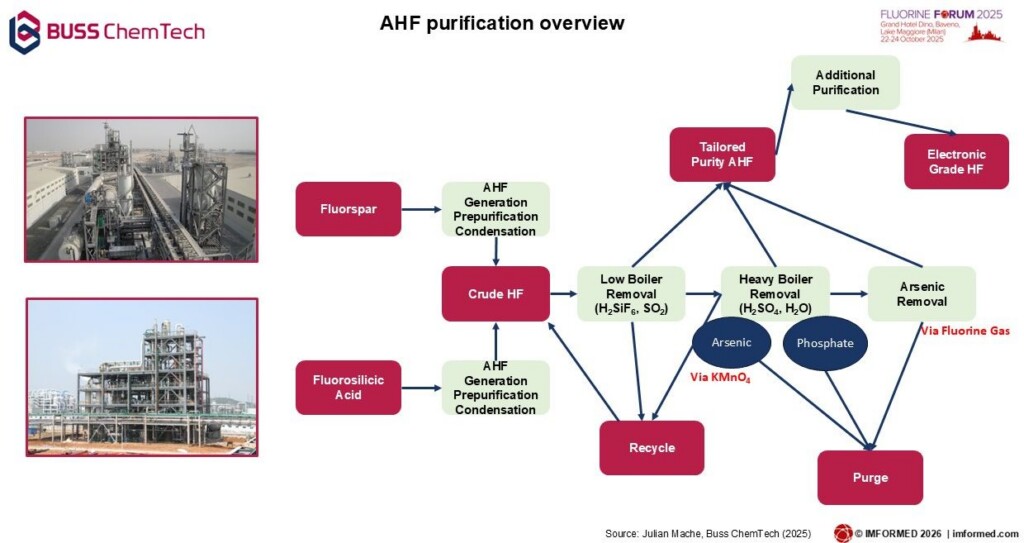

Fluorine technologies: Novelties in HF purification

Julian Mache, Technology Manager Fluorine, BUSS ChemTech AG, Switzerland

Mache highlighted the main AHF impurities as being:

- Water – Downstream reactants and catalysts can be water sensitive

- SO2, SO3, H2SO4

- SiF4: Reduces quality of aluminium if present in AlF3

- Arsenic – poisons catalyst in downstream processes; acts as wrong dopant in semiconductors

- Phosphates – poisons catalyst in downstream processes

Key steps are then required in its purification: generation of crude HF; low boiler distillation; high boiler distillation; followed by additional high purity steps.

Features of technical and electronic AHF grades were examined, along with technical and analytical challenges.

FLUOROCHEMICALS | NEW ENERGY | BATTERIES

Fluorochemicals review and market outlook

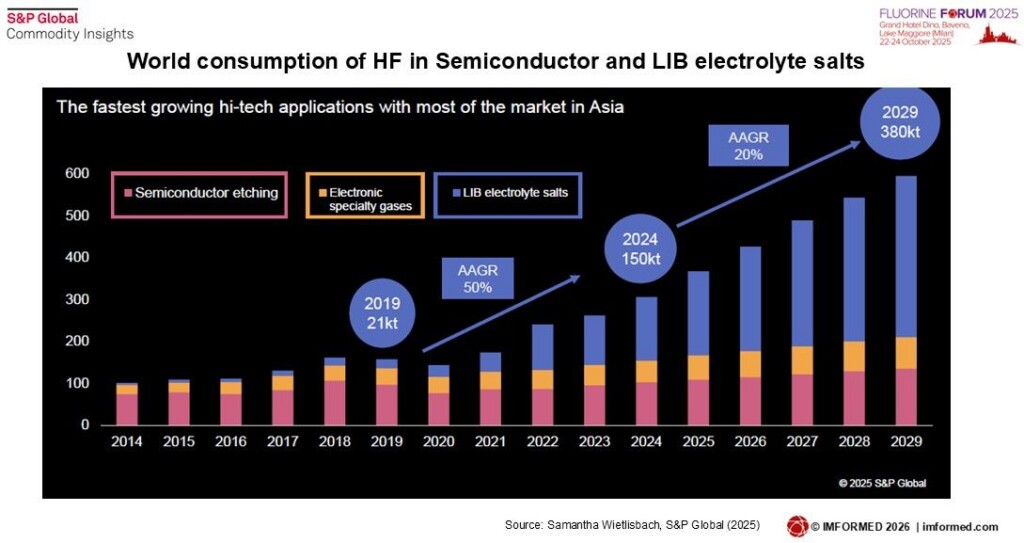

Samantha Wietlisbach, Head of Inorganics and Minerals Research, S&P Global Commodity Insights, Switzerland

In her usual excellent and comprehensive review, Wietlisbach focused on fluorine raw materials production and consumption, a focus on FSA, aluminium fluoride raw material developments and downstream demand outlook, a hydrofluoric acid trade update, demand for inorganic fluorochemicals, and a fluoropolymers overview and PFAS demand consequences in Europe.

Attention was drawn to the increasing role of inorganic fluorine chemicals used in electronics and batteries. World consumption of HF used in semiconductors and lithium-ion battery electrolyte salts is forecast to grow to 380,000 tonnes by 2029.

Among the key takeaways were:

- Diversification of fluorine supply. FSA becoming a significant source of HF

- Li-ion batteries for EV driving growth of HF

- EV adoption slowed down in 2023, but the long-term outlook is positive

- PFAS regulations will change the fluoropolymer landscape in the EU and other regions

- Many domestic fluoropolymer uses will be severely impacted from 2027 onward

HF in new energy applications

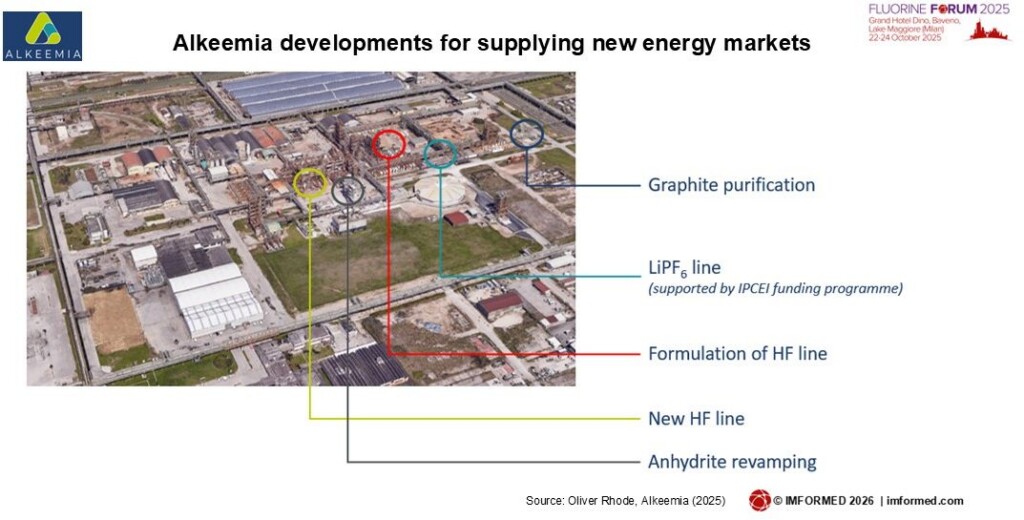

Oliver Rhode, Director Business Development, Alkeemia SpA, Germany

Rhode introduced Alkeemia as one of the largest European producers of HF, supplying fluoropolymers, refrigerants, agrochemicals, electronics, metallurgy, construction and glass markets.

The company is embarking on some exciting new developments including graphite purification, a LiPF6 production line, a new HF line, and anhydrite revamping.

HF applications in new energy were highlighted, including batteries for EV, energy stationary storage, defence applications, portable electronics, electric speciality gases, and photovoltaics.

Rhode outlined the key factors influencing HF demand in new energy markets as:

- China – dominating fluorspar and HF industries

- Independence from Chinese supplies

- Penetration of electric vehicles

- Development of battery technologies (EV, ESS)

- Development of traditional applications

- HF-market consolidation in Europe

- Fluorspar recognized as “critical mineral”

- FSA

- Macro-economic developments

- Policy risks

- PFAS in Europe

In terms of HF and EV markets, Rhode considered that China should be treated as “disconnected” from the world – “In battery technology, China is approx. eight years ahead of the rest of the world” he said.

There is significant HF production overcapacity in China. In 2024, 15% of HF consumption in China was linked to new energy applications (production of HF 1.7m tonnes). Also, overcapacity in LiPF6 manufacturing: some 250,000 tpa capacity for <200,000 tpa demand.

Considering the key factors affecting the supply-demand-balance of HF, Rhode forecast that an additional 500,000 tonnes of HF would be required to meet demand by 2030.

However, while sufficient HF capacity is already installed to support this growth in new energy applications in China, this is not the case in the rest of the world. Outside of China, Rhode considered that the bottleneck to support the growth in new energy applications was HF capacity, and not fluorspar.

Scaling-up HF-free production of fluorochemicals: New routes towards Li-ion battery electrolyte salts

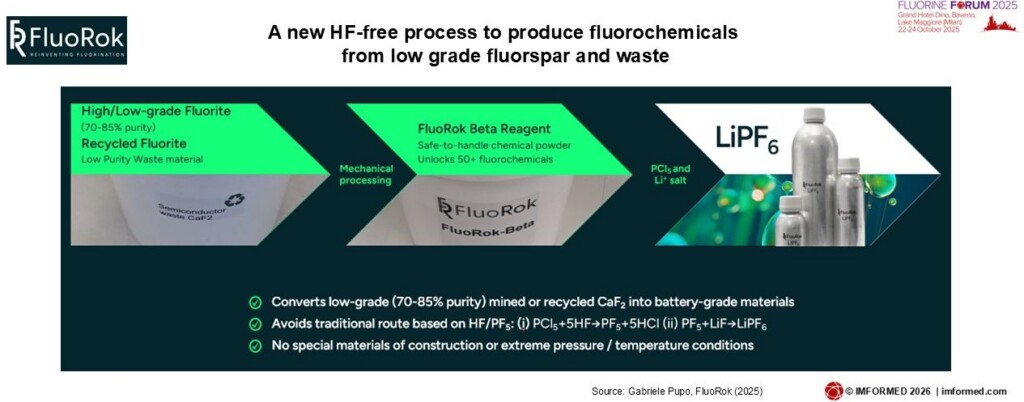

Dr Gabriele Pupo, CEO, FluoRok Ltd, UK

Pupo explained how FluoRok “rethinks” fluorochemical manufacturing with a new disruptive innovation that is low cost, using low carbon technology, and unlocks localised production.

FluoRok’s novel method for chemical activation of fluorite is HF-free and utilises a “FluoRok Beta Reagent”. The proprietary process converts low-grade (70-85% CaF2 purity) mined or recycled CaF2 to high-purity fluorochemicals; avoids the creation, handling and storage of HF; with no special materials of construction or extreme conditions.

It can also be applied to converting polyfluorinated (PFAS) materials waste/scrap into high-purity fluorochemicals.

With increased demand for Li-ion batteries, FluoRok is targeting the lithium hexafluorophosphate LiPF6 electrolyte market with its new process.

SEMICONDUCTORS | CEMENT | NUCLEAR

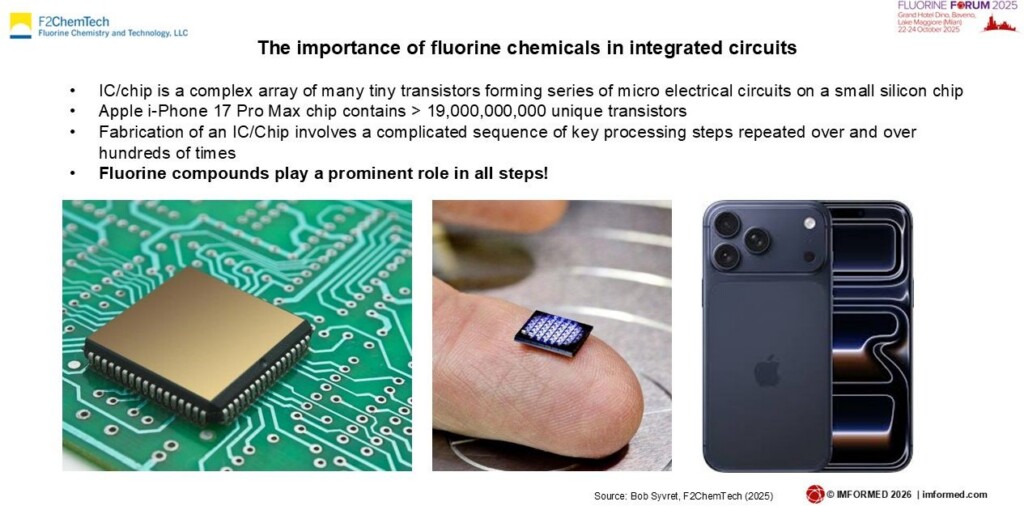

Fluorochemicals with irreplaceable applications in semiconductor materials processing

Dr Robert Syvret, Owner, Fluorine Chemistry and Technology, LLC, USA

The various applications of fluorine products in semiconductor manufacturing is not often clear. Here, Syvret shone a welcome light on: Importance of semiconductor materials; Key process steps used in building an IC device; Importance of fluorocarbon compounds in key IC process steps; and Production of fluorocarbon products for today’s semiconductors.

Syvret looked at the growing semiconductor market and its main drivers. In 2024, the total global market was US$630.5bn and showed an annual growth rate of >14% from 1980 to 2024.

Key takeaways:

- Semiconductors are an integral part/enabler of modern society

- Strong market and growing demand fuelled by explosion of data with no end in sight

- Fluorochemicals are essential to the production of semiconductor materials and IC devices at every stage of manufacturing

- Fluorochemicals are irreplaceable for plasma etching

- Fluorochemicals are irreplaceable for chamber cleaning

- Fluorochemicals are irreplaceable as deposition precursors

- All fluorochemicals used for semiconductor manufacturing are high value products derived ultimately from HF

- Everything is traced back to the essential minerals fluorspar and fluorapatite

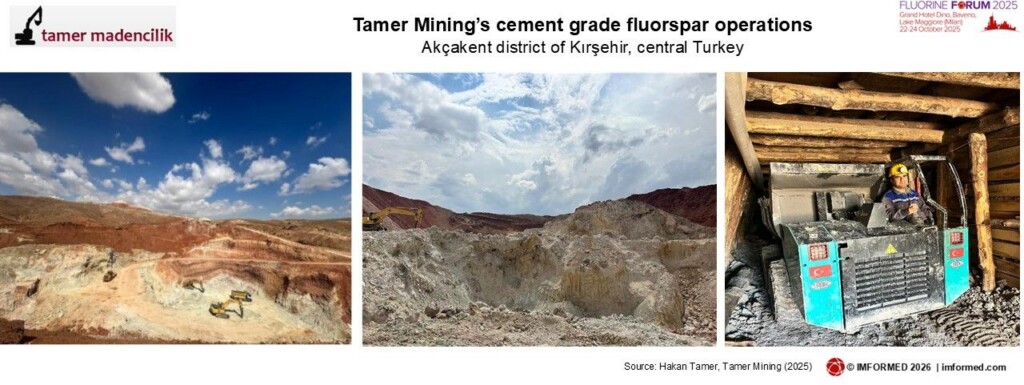

Fluorspar usage in cement production

Hakan Tamer, General Manager, Tamer Mining, Turkey

Tamer Mining is dedicated to providing top-tier cement grade fluorspar with its six fluorspar permits hosting “millions tonnes” of fluorspar reserves in Akçakent district of Kırşehir, central Turkey.

Cement grade fluorspar is a vital resource in the construction industry. Key fluorspar applications in cement include:

- Energy Efficiency in Cement Production: Fluorspar reduces the temperature required to form clinkers, the primary ingredient in cement. This leads to significant energy savings and lower fuel consumption, making the production process more cost-effective.

- Durable Cement Products: The addition of fluorspar improves the strength, compressive resistance, and durability of cement, making it ideal for use in large-scale construction projects like bridges, dams, and skyscrapers.

- Sustainability in Construction: Fluorspar enables the cement industry to reduce its carbon footprint by lowering fuel usage and CO₂ emissions, supporting green building initiatives and circular economy practices.

While cement grade fluorspar has a lower purity level than its acid-grade or ceramic-grade counterparts, its “impurities” are far from a disadvantage. In fact, specific impurities like silica and alumina can actively complement the cement-making process.

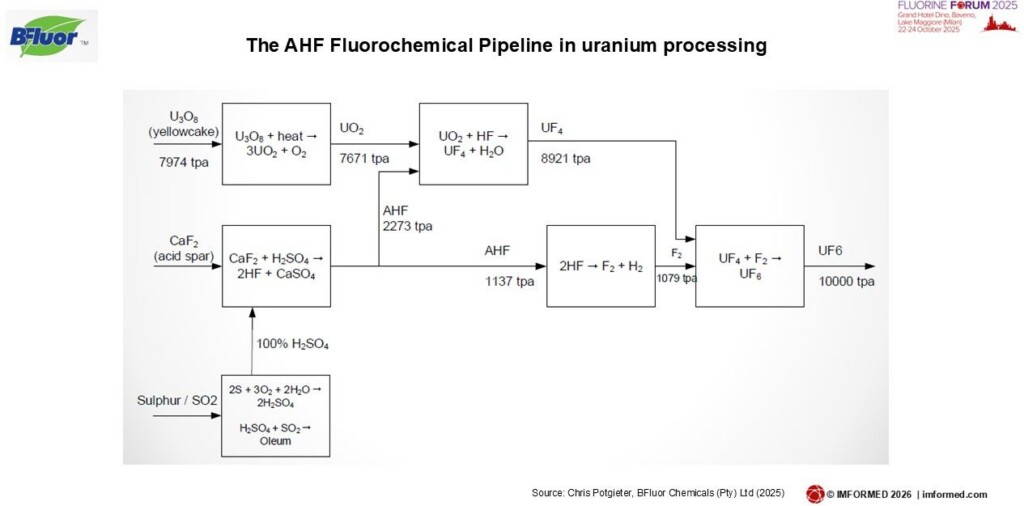

Nuclear renaissance & the impact on the fluorochemical value chain

Chris Potgieter, Director Business Development, BFluor Chemicals (Pty) Ltd, South Africa

Potgieter covered the expected growth in nuclear fuel production, the downstream impact of fluorochemical Industry growth, and bridging the value chain gap.

Nuclear fuel production is forecast to grow owing to increasing demand driven by new reactor construction and extended lifespans, to >100,000 tU by 2040.

In the process route from uranium refining (yellow cake U3O8) to UF6, 100,000 tpa UF6 provides for about 34,000 tpa HF demand.

Conclusions were:

- Major opportunities are sprouting from the stimulating and catalytic impact coming from the expected nuclear renaissance

- Will have to be drawn by growth in offtake on financially viable HF kilns

- Geographic intersection points of the two value chains, in the context of supply chain logistics (ease of transport of intermediates and products) are the focus areas to unlock opportunity

The informal Roundtable Networking Session was as popular as ever, where delegates could relax, network, and share insights at themed and hosted Roundtables; almost as popular was the very tasty cake kindly baked by the Grand Hotel Dino for IMFORMED’s 10th Anniverary!

Many thanks and hope to see you at Fluorine Forum 2026, Baveno, 26-28 October

Special thanks from IMFORMED to Fluorine Forum 2025 sponsors FLUORSID and SPAETER raw materials, exhibitors Rio Tinto and Steyuan Mineral Resources Group Ltd, and all our supporters, speakers and delegates for their fine participation and support.

Looking forward to meeting you again later this year at Fluorine Forum 2026, Baveno, Lake Maggiore (Milan), 26-28 October.

Missed attending Fluorine Forum 2025?

A full PDF set of presentations available for purchase.

Please contact Maria Bernard T: +44 (0) 208 153 0035 maria@imformed.comAnd why not book now with our attractive Early Bird Rates for…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment