Two weeks to go until Fluorine Forum 2019

![]()

With just under two weeks until IMFORMED’s Fluorine Forum 2019 at the Alcron Hotel, Prague, on 21-23 October, the great and the good of the global fluorine raw materials supply chain are readying themselves for two days of exceptional presentations, discussion, and networking.

In recent months the fluorine raw material supply market has had a several significant developments which are already raising questions and comments with regard to 2020 and beyond.

SepFluor Ltd in South Africa announced the official start-up of its Nokeng Fluorspar Mine and Plant Project in August and commenced loading its first 2,000 tonnes of acidspar on 24 September for European customers via Rotterdam.

The mine’s concentrator is designed to produce around 180,000 tpa of acid grade fluorspar (97% CaF2) and 30,000 tpa of metallurgical grade fluorspar from run-of-mine fluorspar ore production of 630,000 tpa.

SepFluor completed its Nokeng Fluorspar Mine and Plant in August (top) while in September a first shipment of 2,000 tonnes acidspar was loaded, to go by road to Durban, then to Rotterdam (bottom) “This is a key milestone for the company and we remain focused on the successful ramp-up of operations towards nameplate capacity’” said CEO, Rob Wagner. Courtesy SepFluor

Canada Fluorspar Inc (CFI) now appears unlikely to reach its nameplate acidspar capacity of 200,000 tpa acidspar concentrate at St Lawrence, Newfoundland, before the end of the year owing to technical issues.

Meanwhile, GFL GM Fluorspar SA, a subsidiary of Gujarat Fluorochemicals Ltd (GFL), India, is to expand production capacity of acid grade fluorspar at its Taourirt operation in Morocco.

The mine and beneficiation plant have been operational since 2018 with a capacity of 40,000 tpa acidspar, which is now planned to be increased to 60,000 tpa, expected to be complete by Q2 2020 (see New fluorspar source for European markets).

GFL GM Fluorspar’s open pit mine is located on the western slope of Jebel Tirremi, 10km north-west of Taourirt, Taourirt province, Morocco. Courtesy GFL

Mongolian fluorspar production has experienced a rejuvenation in 2018 and 2019 with increased output taking up the slack from declining Chinese availability, but political changes in the country have complicated and hindered fluorspar investment and development.

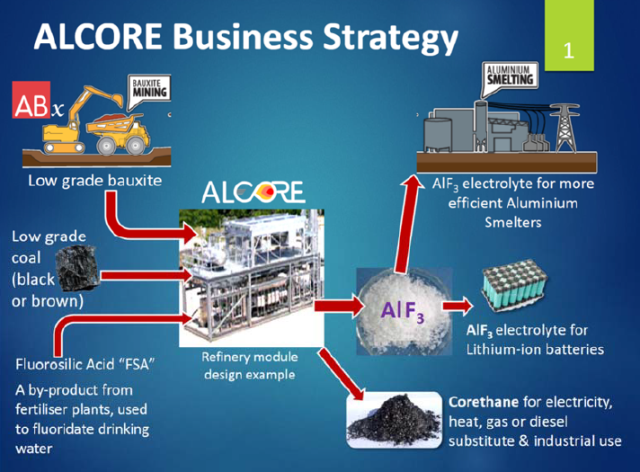

Australian Bauxite Ltd’s (ABX) wholly-owned subsidiary, ALCORE Ltd has achieved production of test samples of aluminium fluoride (AlF3) and several valuable co-products at its pilot plant in Berkeley Vale, New South Wales. Grades produced ranged 31.1-35.8% Al, 54.8-60.3% F.

This is an ongoing project by ABX to develop bauxite deposits in eastern Australia and Tasmania, which includes AlF3 production from low grade bauxite for aluminium smelters and Li-ion battery manufacturing.

In early September, leading fluorspar and fluorochemicals group Mexichem announced a major restructuring and name change: Mexichem’s corporate name has been changed to Orbia Advance Corp., headquartered in Boston, and Mexichem Fluor has become Koura Global.

Described as a “Human-Centered Business Transformation” the move reflects a year-long process to transform the company into a “future-fit, human-centered organisation… to address the challenges that define how people live and thrive today and in the future.”

In addition to the fluorspar business, Orbia is a world leader in speciality products and innovative solutions across multiple sectors of industry and commerce, from agriculture and infrastructure to telecommunications, and healthcare.

Key among the leading discussion topics at Prague will be:

- The changing role & performance of Chinese fluorspar supply & markets

- Ramifications of the latest round of environmental inspections affecting Chinese fluorspar and HF production

- Mongolia’s fluorspar future & trade with China and the world

- Which new world supply sources are emerging and when?

- How the world market will absorb new supply

- Is clarity on accurate world fluorspar consumption achievable?

- Changing demands for F compounds in the cooling markets

- How will growth in Li-ion, and maybe F-ion, batteries affect acidspar demand and price?

- Influence of trade wars & recession-hit industries on demand

- Impact of illegal HFC trade on EU emissions targets

- FSA processing & technologies to consider as real alternatives

Programme update: enter New Chemical Products, Russia

Owing to a late speaker drop-out, the Fluorine Forum 2019 programme has been updated with a slight alteration on Day 2 in order to accommodate a new speaker on a most exciting topic for the market.

IMFORMED is delighted to welcome Bob Welch, Sales Director, New Chemical Products LLC, USA to present on “A new proven technology to recover Anhydrous HF from FSA”.

Accompanying Bob will be Anton Mamaev, President, New Chemical Products, who will be participating in the Alternative Sources Roundtable.

Following the Welcome Reception, kindly sponsored by SepFluor Ltd, and featuring local musical entertainment, we have two full days of presentations and discussion:

OVERVIEWS

Key trends and outlook for the fluorspar market

Oliver Rhode, CEO, Xenops Chemicals GmbH & Co. KG, Germany

Trade & tariffs: Where we’ve been and where we might go

Ray Will, Director of Specialty & Inorganic Chemicals Consulting, IHS Markit, USA

MINING & PROCESSING

Cost factor trends in fluorspar processing

Ashok Shinh, Ashok Shinh Consultancy Ltd, UK

Fluorspar mining in Europe: mineral waste (tailings) management in a National Park

Peter Robinson, Chairman, British Fluorspar UK Ltd, UK

Fluorspar mining in the Czech Republic

Vít Kučera, Managing Director, Fluorit Teplice s.r.o., Czech Republic

SUPPLY: VIETNAM | CHINA

Nui Phao: Striving to be the best-in-class supplier

Craig Bradshaw , CEO, Masan Resources Group, Vietnam

The development of China’s fluorspar industry

Usman Khan, CEO, Kcomber Inc., China

China’s fluorspar market update

Liao Xinhua , Chairman, CNMIA Fluorspar Committee, China

MARKETS 1: REFRIGERANTS

The evolution of refrigerant gas and the role of Chemours in the market

John Zielinski, Executive Buyer Fluoroproducts, Chemours, USA

Changes in refrigerant use and its impact on the air conditioning and refrigeration markets

Andrea Voigt, Director General, European Partnership for Energy & the Environment, Belgium

MARKETS 2: HF & FSA DEVELOPMENTS

HF and fluorine developments in Saxony and eastern Europe

Johannes Scheruhn, General Manager, Scheruhn Minerals and Chemicals GmbH, Germany

HF from Fluorosilicic Acid (FSA): challenges and opportunities

Datta Umalkar, Technical Consultant, Chenco GmbH, Germany

A new proven technology to recover Anhydrous HF from FSA

Bob Welch, Sales Director, New Chemical Products LLC, USA

MARKETS 3: FLUOROCHEMICALS | ALUMINIUM FLUORIDE

India: An emerging market for acid grade fluorspar

Bimlesh Jain, Executive President (Corporate), Gujarat Fluorochemicals Ltd, India

Downstream markets for fluorochemicals, through to fluoropolymers & fluoroelastomers

Samantha Wietlisbach, Principal Analyst, Chemical, IHS Markit, Switzerland

Trends in aluminium fluoride supply and demand

Adam Coggins, Analyst, Roskill, UKPlus, our acclaimed Roundtable Networking & Discussion session with table themes on China,

Alternative Sources, Processing Cost Factors, Aluminium Fluoride and Fluorochemicals.Click here for full details and timings

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}