Mineral supply chain and market competition awareness urged

One of industrial minerals’ key consuming markets, refractories, is expected to undergo a period of slow growth for the next few years, meaning at least steady, if not reduced, demand for refractory minerals.

RHI AG’s Weissenstein magnesite mine, Austria, supplies feedstock for dead burned magnesia used in refractories

The steel industry is the main driver for refractories, consuming 70% refractory bricks and monolithics, and is projected to grow by a mere 0.5-1.8% in the next few years, according to Hans Jürgen Kerkhoff, President of the German Steel Federation.

Speaking at the opening session of last week’s UNITECR 2015 in Vienna, the biennial gathering of the world’s refractories industry, Kerkhoff warned that the industry should be adapting to the “new normal” of steel production performance, ie. a low growth period, following many years of increasing output.

Kerkhoff highlighted China’s domestic steel market as “saturated”, with its steel production having peaked and now in decline for the first time in 25 years.

The concern here is that Chinese exports of low cost steel are increasing, especially to nearby Asian markets such as India, and thus impacting the domestic growth, and in turn, refractory demand, of other Asian steel industries.

Indian steel potential challenged

India has been cited many times as the future driver of world steel growth, with some 125-130m tonnes of crude steel forecast to be produced by 2020, representing a massive growth of 14.1%.

However, there are major challenges facing the Indian industry including cheap imports taking 30% of the steel market (with 9m tonnes from China expected for 2015), and low quality refractories used in induction furnaces currently representing 30-35% of Indian steel production.

In his presentation on the Indian steel industry, Dr A.K. Chattopadhyay , Managing Director, Vantage Refractory Technologies, National Refractories, India, said that with the onset of Total Refractories Management, the onus is on the refractory makers to supply, install and maintain the refractory linings.

However, while on the one hand this beckons new business opportunities (and certain overseas refractory companies have been and are continuing to invest in India), on the other hand Dr Chattopadhyay lamented that the refractory makers are kept in the dark by many users about various operating parameters which affect refractory lining life.

Another factor impacting the domestic refractory industry is the government policy of making the import duty of refractory raw materials the same rate as finished refractory products.

Mineral supply chain & market competition

In his keynote presentation, Andus Buhr, Global Technical Director Refractories, Almatis GmbH, described refractories as “the tools for steelmaking”.

It is true that without refractories, you cannot have steel; but without industrial minerals, you cannot have refractories.

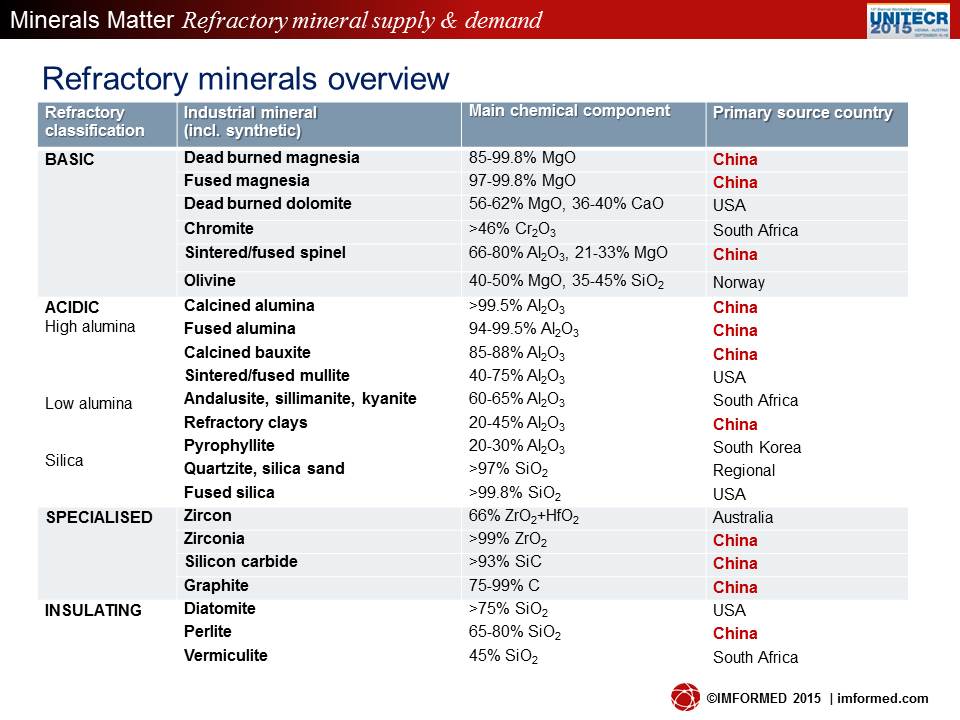

Some 20+ industrial minerals are the “DNA” or building blocks essential to producing refractory products. In 2014, it was estimated that some 35m tonnes of refractory minerals were consumed (Richard Flook & Ted Dickson (2014)).

Refractory minerals maybe classified into basic, acidic, specialised, and insulating categories, but each mineral will have is own supply chain characteristics. This was the subject of the UNITECR 2015 presentation by Mike O’Driscoll, Director, IMFORMED – “Minerals Matter: Refractory Raw Material Supply Trends & Developments” (Presentation PDF download).

There are two crucial factors often overlooked when sourcing certain refractory minerals:

1. their relatively limited sources of supply, and

2. competition in their demand for use in markets other than refractories.

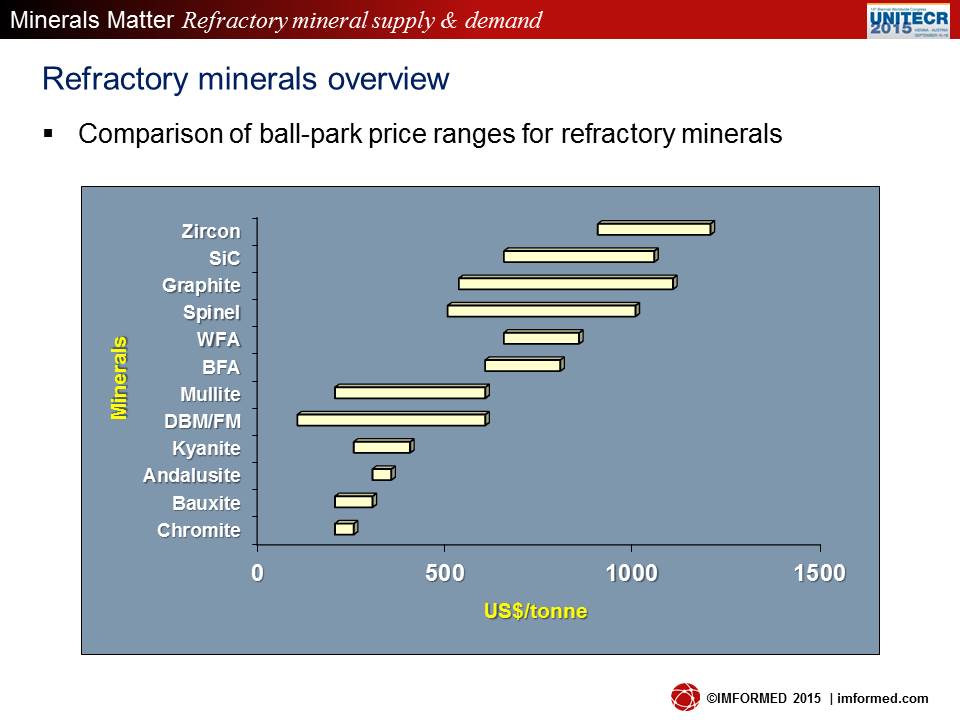

As indicated in the chart above, China appears as the primary source of many refractory minerals. Indeed, China is the dominant supplier (>50% world supply) of bauxite, brown fused alumina, flake graphite, fused magnesia, and silicon carbide (and >44% dead burned magnesia).

Certain minerals have very few sources: refractory grade bauxite supply is limited to China and Guyana (the latter operated by Bosai Minerals Group, China); andalusite supply is limited to South Africa, France, and Peru, with Imerys dominating operational management at some 60% (potentially increasing to 84% should the ongoing appeal against its blocked acquisition of Andalusite Resources turn in its favour).

Limited supply sources, particularly in locations remote from refractory markets, also impact on logistical costs and considerations. This is significant, since in the main, industrial minerals are low value, high volume commodities, where logistics costs can represent >50% of the delivered mineral price.

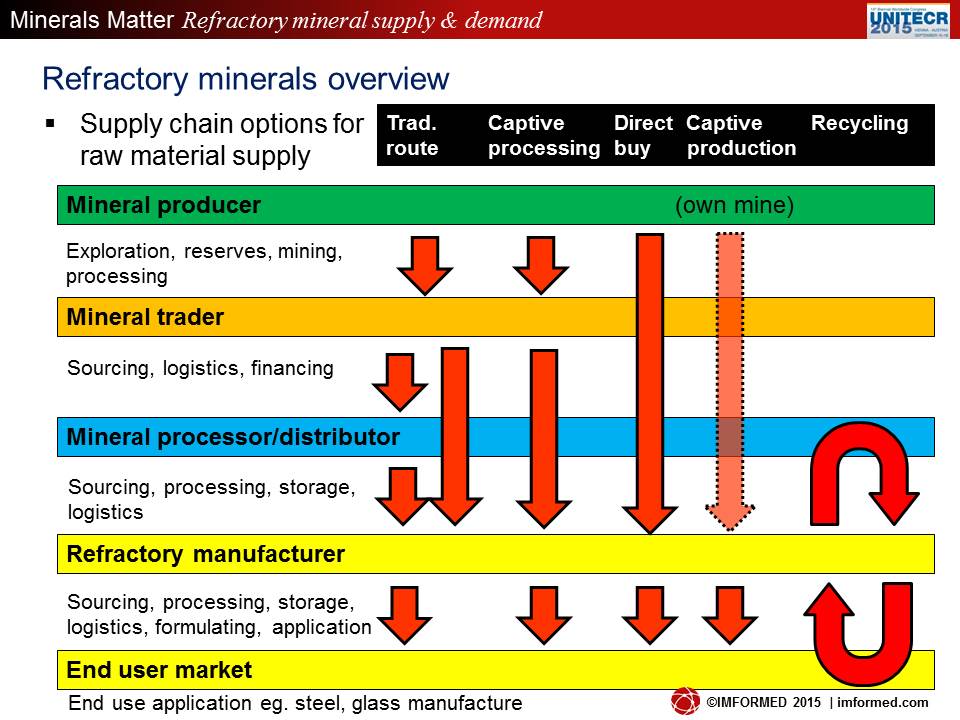

There are several supply chain routes from mine to market for refractory minerals. Over the last ten years the traditional routes from mine via traders/processors to end user have been supplemented by direct buying, captive production, and increasingly, recycling of refractories.

These more recently established supply routes are not for every refractory manufacturer. The main examples of increasing vertical integration have come from the large magnesia consumers (and producers) RHI, Magnesita, Magnezit, and Kumas, each of which had mining as an original core business. Many Chinese producers of bauxite, magnesia, and fused alumina are also fully integrated.

While there may yet be more moves in vertical integration within the majors, it is the refractories recycling sector which is going to see more activity and growth, as certain mineral processors start to specialise in recycling not just spent refractories, but other industrial wastes that yield “secondary raw materials”, such as steel slag, fly ash, aluminium salt dross.

Eventually, these secondary raw materials will become a standard option for refractory raw material purchasers.

Learn all about Secondary Raw Materials sourcing, supply, and market applications at Mineral Recycling Forum 2016, 14-15 March 2016, Rotterdam. Register before 31 December 2015 for major savings.

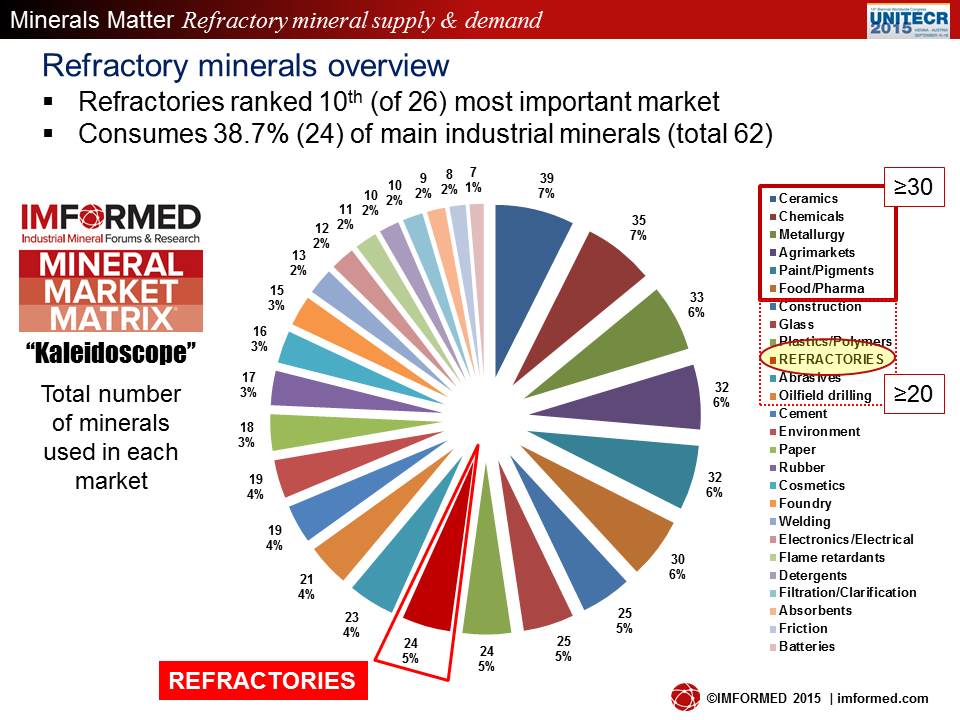

In research conducted by IMFORMED, we compiled a Mineral Market Matrix® to illustrate at a glance which minerals are used in which markets. The refractories market ranks 10th out of 26 leading markets, using some 24 different minerals.

Markets using more minerals than refractories include ceramics, chemicals, metallurgy, agrimarkets, food/pharma, construction, glass, and plastics/polymers (see chart).

The point is that minerals used to make refractories are also in demand for other manufacturing industries, and in some cases this impacts on raw material availability causing shortages.

With the present oil price depression, demand for ceramic proppants has declined considerably. However, many bauxite producers in China, and bauxite project developers outside China (eg. First Bauxite, Guyana), had modified strategies to exploit bauxite for ceramic proppant manufacture as well as for refractory grades (or instead of, in the case of First Bauxite). This scenario could still unfold when oil prices recover.

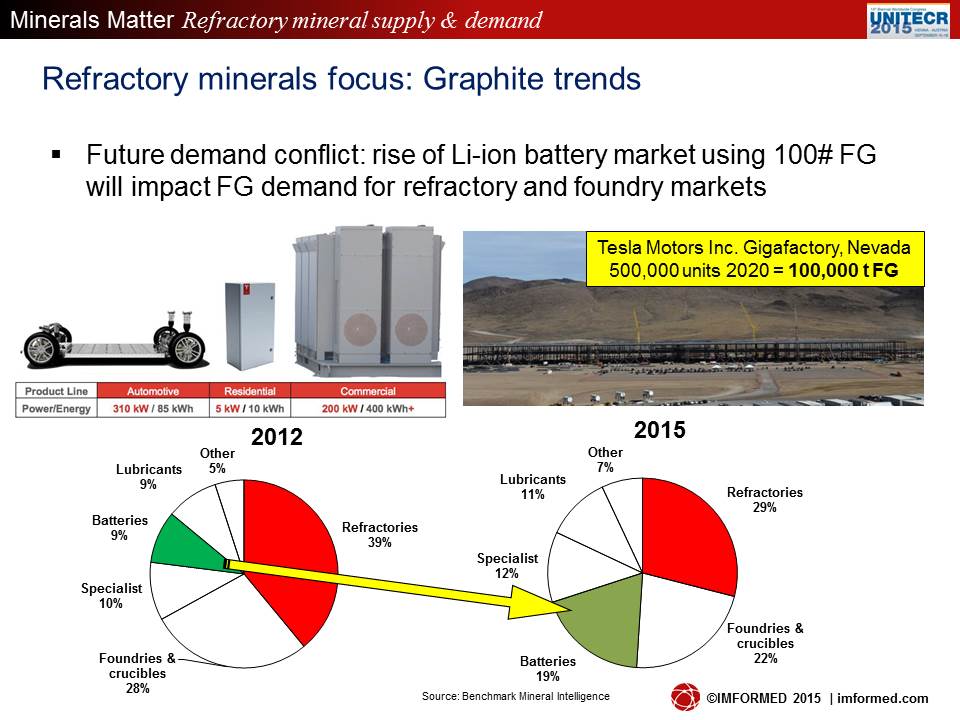

Perhaps the most interesting potential example of market competition impinging on a refractory mineral’s supply availability is graphite.

World flake graphite production estimates range 400-500,000 tpa, and supply is dominated by China (about 60%), followed by just a few other countries which are mostly limited to supplying local/regional markets.

Refractories consumption accounts for just under a third of flake graphite consumption, according to Benchmark Mineral Intelligence. However, it is the rapid rise of the battery market for flake graphite (used as a precursor raw material to make spherical graphite used in Li-ion battery anodes), which is significant, having more than doubled from 2012 to 2015, now holding a 19% market share.

This is expected to grow further with the advent of enhanced demand for Li-ion batteries used in electric vehicles, utility storage units, and consumer devices. For example, should Tesla’s Gigafactory in Nevada come to full capacity of 500,000 units by 2020, this will require an estimated 100,000 tpa of flake graphite. A future strong competitor for refractory graphite?

Mineral supply trends and outlook

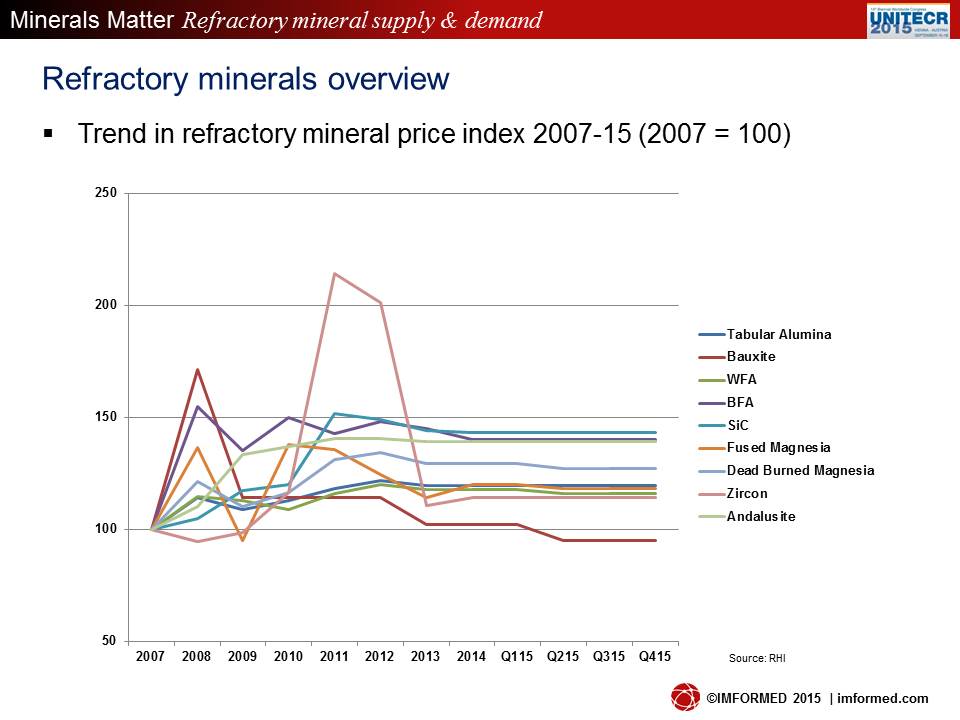

Without doubt, the present market for refractory mineral supply is one of oversupply and depressed prices – it’s a buyer’s market.

Most refractory mineral purchasers interviewed by IMFORMED agreed that prices were low, and expected to remain so into 2016, and most raw material was readily available.

This is not only down to the slump in world steel, glass, and cement production dictated by an overall economic slowdown, but in particular to the acute recession in China. China’s market downturn has decimated the domestic refractories and refractory mineral supply market.

Compounded by production sector consolidation and environmental controls, many Chinese refractory mineral producers are producing at cost price or going out of business altogether.

On the one hand, this may free more raw material available for export, but on the other, it may mean a major cut, or at least uncertainty, in future Chinese mineral supply if/when the market recovers. How many of the recently closed or reduced capacity operations will re-open or ramp up capacity?

This is where the drive for developing mineral projects outside China is retaining some momentum – particularly for graphite, where three projects have now reached production stage and others are coming very close; and to a lesser extent magnesite, where most projects are at very early stages.

The depressed refractory mineral prices are clearly barriers here and now, but interest in developing a range of such projects persists, especially if market conditions can only go up and China’s recovery is not coming anytime soon.

The market situation has also revived plans by established refractory mineral producers to look to diversify into other markets, eg. dead burned magnesia producers Nedmag, the Netherlands (magnesium hydroxide for pulp and paper), Kumas, Turkey (caustic calcined magnesia for cement boards, magnesium hydroxide for high value markets).

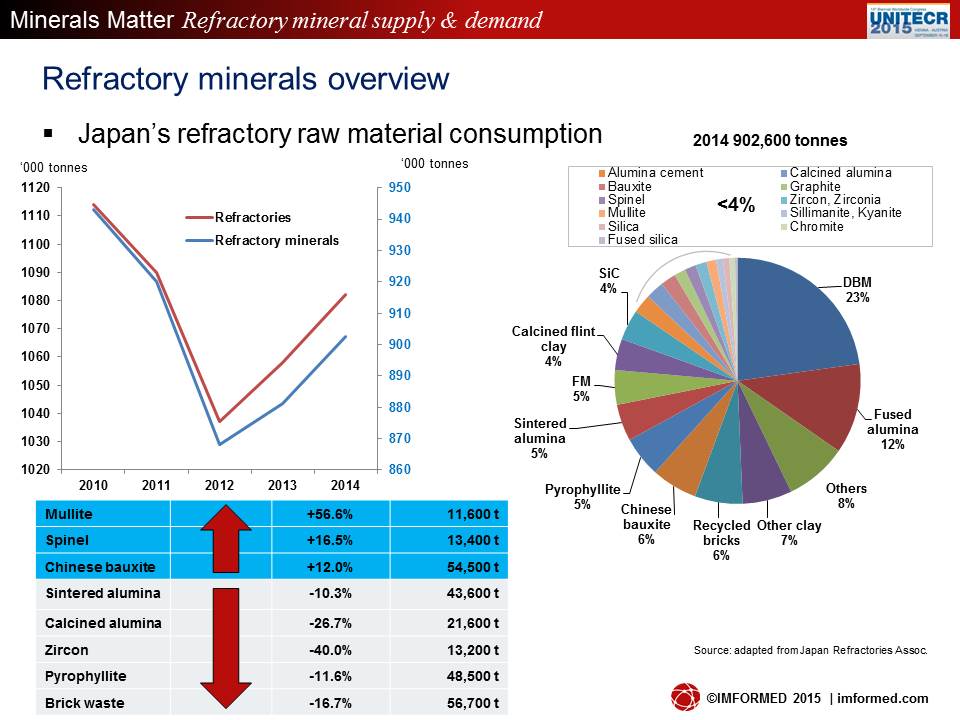

Regarding specific refractory mineral demand, Japan, often viewed as a barometer for the refractory industry, over the last five years has witnessed an increase in consumption of mullite (+56%), spinel (+16.5%), and Chinese bauxite (+12%). Certainly, this chimes with the view that increasing volumes of synthetic refractory minerals will be used in refractories.

In contrast, minerals in decline over the same period included zircon (-40%), pyrophyllite (11.6%), and sintered and calcined alumina (-10.3%, -23.7%).

At UNITECR 2015, Andus Buhr, Global Technical Director Refractories, Almatis GmbH, underlined that the pursuit of cleaner, low impurity steels is demanding higher quality refractories, and in particular, higher alumina and synthetic alumina refractories.

In the 1960s, steel impurity levels were in the order of 600ppm. From 2000 this level has decreased to <100ppm.

More aggressive slags will need higher wear resistant linings, using magnesia-carbon bricks using fused magnesia and perhaps a higher carbon content. Although at the same time, Buhr also acknowledged that there is a trend to reduce carbon pick-up from refractories by reducing the carbon content in refractory products – whether this will have a major impact on graphite consumption in refractories remains to be seen (it might be negligible) – but it needs to be watched (especially by all those projects under development).

There is certainly room for andalusite applications in refractories, although certain delegates with the aluminosilicate mineral close to their hearts clearly felt that Dr Buhr may have been too dismissive of andalusite’s future in refractories.

Buhr said that andalusite bricks had been replaced by high purity spinel bricks at the Ijmuiden steelworks, and that andalusite and bauxite was now primarily used in the back lining and not the wear lining of steel ladles, which is seeing more use of magnesia-carbon, alumina-magnesia-carbon, and synthetic alumina grades.

One other trend mentioned was that of the aim for thinner steel ladle linings. Buhr demonstrated that a reduction of just 10mm in refractory lining of a steel ladle translates to 2.5 tonnes more steel made.

This would naturally have an impact on refractory mineral volumes required in future (contributing to the ongoing decline of specific refractory consumption per tonne of steel, now around 5-10kg/t), but also would clearly require refractories of even higher purity and performance, and thus very good quality refractory minerals.

The future for refractory minerals demand is assured. Mineral do matter. But a weather eye is required from mineral suppliers on steelmaking trends as the main driver, and from refractory raw material purchasers on mineral supply chains and competitive markets.

PDF download of Mike O’Driscoll’s “Minerals Matter: Refractory Raw Material Supply Trends and Developments”

Learn about the latest magnesia supply trends and market developments at MagForum 2016 Magnesium Minerals & Markets Conference, 9-11 May 2016, Vienna. The only conference you’ll need to attend if you’re in the magnesia business. Register before 31 December 2015 for major savings.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Excellent presentation Mike. Peak refractories has certainly arrived and in the short and medium term the refractory emphasis will be more on quality and less on volume. The industrialization of Africa might be the next major stimulus but it is some time off.

Thanks Richard: yes, Africa needs watching; I also think with sanctions being lifted, Iran might be showing some promise for both consuming market as well as mineral sourcing development opportunities.