Mineral Recycling Forum 2017 Review

Rotterdam was again the setting for IMFORMED’s second Mineral Recycling Forum last week, 7-8 March 2017, bringing together leading players in the fast evolving secondary raw materials sector.

A real buzz was felt among the delegates as they listened to experts presenting on a range of topical subjects followed by much discussion and networking during the coffee and lunch breaks.

Perhaps indicative of this Forum’s rationale and growing success, was the comment by Allan Bell, Process Materials Manager, Procurement at British Steel: “Programme items that appeared irrelevant to our industry still offered some food for thought for our by-products.”

For programme, feedback, attendees, and picture gallery, please go to:

Mineral Recycling Forum 2017, 7-8 March 2017, Rotterdam

Such feedback has illustrated the gathering momentum of the industrial mineral recycling business, with common challenges and differing solutions offered whether dealing with slags, spent refractories, construction waste, or waste electrical and electronic equipment.

The upshot has been the emergence of new opportunities to develop mineral products from waste for a range of market applications.

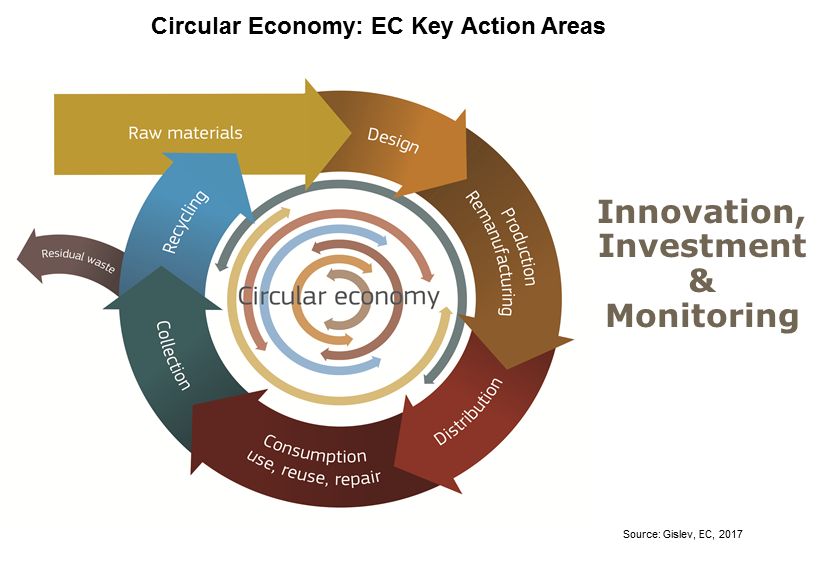

The Circular Economy

Setting the scene in ideal fashion was Magnus Gislev, Policy Officer for Resource Efficiency and Raw Materials, DG GROW, European Commission (EC), with his overview presentation “EU policies on mineral recycling and the Circular Economy.”

“Industry has a key role to play by making specific commitments to sustainable sourcing and cooperating across value chains.” Magnus Gislev, Policy Officer for Resource Efficiency and Raw Materials, DG GROW, European Commission (EC).

Gislev set out the EC’s extensive raft of policies and initiatives with which to drive forward the transition towards a Circular Economy. Central to this is the €650m Horizon 2020 fund allocated for raw materials’ initiatives, including recycling. Also of note is the impending EU Critical Raw Materials update expected mid-2017.

Providing an international dimension, Gislev reminded of the output of the 2030 Sustainable Agenda, the Paris Agreement to combat climate change, and the G7 Alliance for Resource Efficiency.

Gislev underlined the role that must be played by industry: “Making the circular economy a reality will however require long-term involvement at all levels, from Member States, regions and cities, to businesses and citizens. Industry has a key role to play by making specific commitments to sustainable sourcing and cooperating across value chains.” he said.

One way to make such a commitment is within the European Innovation Partnership (EIP) on Raw Materials: already there are a staggering 123 Raw Materials Commitments, comprising 980 partners, with an indicative budget of around €2 billion.

This led neatly to “Strengthening the European raw materials value chain through recycling” by Dr Roland Gauss, Thematic Officer Substitution and Recycling, EIT RawMaterials GmbH.

EIT RawMaterials, launched and funded by the EC, is the largest consortium in the raw materials sector worldwide. It unites more than 100 partners – academic and research institutions as well as businesses – from more than 20 EU countries.

Dr Roland Gauss, Thematic Officer Substitution and Recycling, EIT RawMaterials GmbH outlined the work of several projects including the development of fly ash for the flame retardants market.

Gauss explained EIT RawMaterials’ mission is to boost competitiveness, growth and attractiveness of the European raw materials sector via radical innovation and guided entrepreneurship.

He outlined the work of several projects including the development of fly ash for the flame retardants market: FLAME FLy Ash to valuable MinErals. The aim of the project is to upscale Dusty Plasma Separator technology to unlock vast amounts of high value minerals from fly ashes.

Waste streams: construction, gypsum, glass

In “Waste-to-Product: how to recover value from waste”, Dr Liesbeth Horckmans, Researcher Sustainable Materials Management, VITO NV, explained how VITO was active in some 140 projects, mapping reuse possibilities from waste materials and developing technical solutions for mineral waste.

Horckmans shared results from REFRASORT, the automated sorting of refractory waste for high value recycling using a LIBS sensor based sorting system. Performance of the recycled refractory material was found to be equal or better than reference products.

Although a demonstration unit is operational, Horckmans acknowledged that some more work was required before it could be scaled up commercially in perhaps 2-3 years.

Construction and demolition waste (CDW) is one of the most important waste streams in the EU, with 500-1,000 million tpa generated, representing 31% of total waste production.

Dr Liesbeth Horckmans, Researcher Sustainable Materials Management, VITO NV shared results from REFRASORT, the automated sorting of refractory waste for high value recycling using a LIBS sensor based sorting system.

Horckmans also outlined the HISER project, part of Horizon 2020, Holistic Innovative Solutions for an Efficient Recycling of Valuable Raw Materials from Complex Construction and Demolition Waste.

Christine Marlet, Secretary General, Eurogypsum, presented “From gypsum to gypsum: a circular economy for the gypsum industry” and stated: “Gypsum as such is 100% and eternally recyclable. You can always reuse gypsum because the chemical composition of the raw material in plasterboards and blocks always remains the same.”

Marlet highlighted how Gypsum-to-Gypsum project partners from eight countries had created a cooperative business model for recycling CDW, among other gypsum based waste. The model is established in France, UK, Scandinavia, Belgium, and the Netherlands; is being implemented in Germany and assessed in Spain.

The two main drivers for gypsum recycling in Europe are the difficulty in accessing primary raw material, and the decline in FGD gypsum as coal combustion plants close.

One of the main challenges to gypsum recycling is the comparative cost. Marlet said: “If the recycling gate fee (average €55/tonne) is lower than the landfill costs, (gate fee + landfill tax), then the recycling route is likely to be chosen.”

Other challenges included the very limited data available on plasterboard waste generation, the waste volume consistency, and recycled gypsum quality consistency. “This means that producers are reluctant to invest in the production process if waste generation is uncertain.” said Marlet.

The two key issues at stake (which can also be translated to other waste streams) were identified as the recyclability of the plasterboard waste at the entrance of the recycling plant and the recyclability of the plasterboard itself due to additives. Marlet stressed that this means collaborative technological innovation between recyclers and producers has to take place.

Dietmar Alber, Operations Director, Minerals & Metals Division, Hosokawa Alpine AG presented “Conversion of recycled glass into high value foam-glass products” and went through the process stages of cleaning, sorting, milling, and processing to foam-glass.

Cullet quality specifications for foam-glass are typically: a feedsize max. 60 mm; moisture: max. 5%; CSP-content: max. 3%; organics: < 0.1%; plastics: < 0.03%; metals: <0.005%.

Alber introduced the REDWAVE CS as an efficient sorting machine for waste glass recycling with low space requirement. The sorting unit removes ceramics, stones, porcelain and metals from the glass stream.

The main ultrafine grinding equipment is a Super Orion Ball-Mill SO-CL and Air Classifier ASP.

Market applications for foam-glass include foam-glass gravel (typically 90% <75-100µm): eg. insulation material for road construction, or concrete foundations; expanded glass balls (99% <36µm): eg. insulation filler for mortars, concrete; and foam-glass boards (97% <15-20µm): insulation boards for the building industry.

“Building waste: construction materials from your waste” by Eunan Kelly, Area Business Development Manager, CDE Global Ltd showed just how much we depend on sand in a range of construction products.

One of CDE Global’s Advanced Recycling Process plants for recovering silica sand from CDW. Courtesy CDE Global

The increasing rate of urbanisation worldwide means that we consume around 50bn tpa of sand.

Until recently, processes for recycling sand failed to deal with lightweight contaminants, organics, clay contamination, and high fines content. Thus CDE Global as evolved an Advanced Recycling Process incorporating aggregate screening, scrubbing and sizing, sand washing and classification, primary stage water treatment, sludge management, and feed system.

“Our projects are diverting more than 13 million tonnes of C&D waste from landfill every year with plants across the UK, Germany, Norway, Australia, India, and Aruba.” said Kelly.

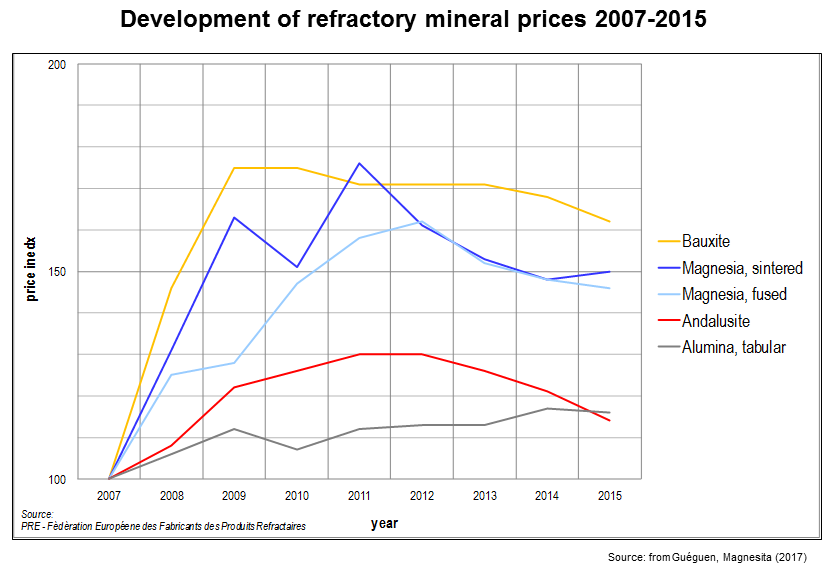

“Raw materials represent 40-50% of the cost of refractories” Dr Erwan Guéguen, Technical Director EMEA, Magnesita Refractories

Refractory recycling

In his presentation “Refractories recycling: technical challenges and market drivers”, Dr Erwan Guéguen, Technical Director EMEA, Magnesita Refractories, provided an excellent overview of where the industry is at present.

Guéguen reviewed the key refractory minerals consumed and how their prices have trended, mostly upwards, in recent years helping to drive recycling. “Raw materials represent 40-50% of the cost of refractories, and China is currently the main supplier of a high volume of important refractory grade raw materials.” said Guéguen.

Other increasing cost factors for refractory manufacturers include energy and environmental control. While producers are aiming to integrate and keep costs down using captive raw materials, the objective is the development of a supply chain for obtaining used refractory materials that can be successfully processed and used for refractory brick production.

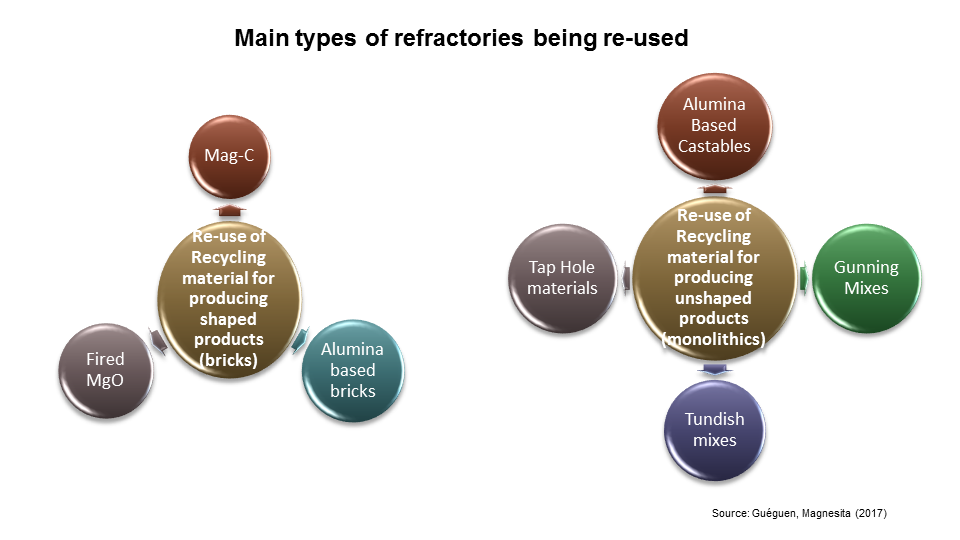

Guéguen highlighted successful recycling of MgO-C bricks and concluded: “We must promote usage of recycling to end users: it is Performance versus Cost; while the price difference between recycling and fresh raw material must make it attractive.”

“Sustainable refractory management” by Ulf Frohneberg, General Manager, Refractory Division, STEULER-KCH GmbH, explained how the company underwent a rethink and rebranding of its recycled products to better inform customers of the benefits and high quality of recycled refractories.

“By the controlled use of professionally recycled raw materials we have continued to further develop our products while keeping the highest quality standards and even improving the performance over many years” said Frohneberg.

STEULER has partnered with refractory recycler Horn & Co. Group to implement what is describes as Sustainable Refractory Management.

“Our end user industry belongs to the main recyclers themselves and is already investing essential budgets in sustainability. Sustainable Refractory Management – which reduces the carbon footprint, preserves finite resources, and reduces waste disposal – will be a part of an even more integrated policy evaluating suppliers and their products.” said Frohneberg.

Processing: spent pot linings, fly ash, waste dust

“Co-processing of spent pot linings from aluminium smelting in cement kilns: lessons learned” by Dr Christian John Engelsen, Senior Research Scientist, Foundation for Scientific & Industrial Research (SINTEF) took the audience through aluminium and cement production, lessons learned in co-processing technology, and the potential of using spent pot linings (SPL) in cement production.

“Huge amounts of SPL are generated annually and stockpiles exist in many countries. Some cement companies have discovered that the benefits outstrip the challenges.” Dr Christian John Engelsen, Senior Research Scientist, Foundation for SINTEF

About 58 million tonnes of aluminium was produced in 2015, which generated some 1.45 million tonnes SPL. Engelsen explained that co-processing in cement manufacture was partly substituting the coal fuel with alternative fuel (AF) and/or the raw materials with alternative raw materials (AR), such as SPL.

Engelsen outlined a successful project in Norway where 97.3 tonnes of pre-crushed refractory (SPL <40 mm) was fed to the raw mill, crushed, and blended with the other raw materials and fed to the kiln during production of high strength cement.

Results showed that refractory SPL provided enough aluminium and substituted the normal Al-source, there were no process or quality problems caused when 5 tph were fed to the raw mill (about 2% of raw feed).

“The potential of recycling raw material resources from SPL refractories is worthy of consideration by the cement industry. Huge amounts of SPL are generated annually and stockpiles exist in many countries. Some cement companies have discovered that the benefits outstrip the challenges.” said Engelsen.

Recovering SPL at a plant in Norway for co-processing in the cement industry Courtesy SINTEF

“Beneficiation will play a key role in securing future supplies of quality assured fly ash for high value cementitious applications” was how Herve Guicherd, Director Business Dev. Minerals, ST Equipment & Technologies LLC, introduced his presentation “Beneficiation: Securing future supply, processing fresh fly ash and reclaiming landfilled ash”.

Guicherd began by outlining the changing world energy mix and the pending closure of coal-fired power stations, before detailing STET’s triboelectrostatic separation technology utilised in fly ash beneficiation (ProAsh), and its benefits in ammonia and carbon removal.

Herve Guicherd, Director Business Dev. Minerals, ST Equipment & Technologies LLC noted that processed landfilled ash can be a valuable source with over 1.7 billion tonnes of fly ash present in landfills.

More than 15 million tonnes of ProAsh has been produced at 14 different power plants worldwide, which is consumed in cement and concrete applications.

With the advent of low “fresh ash” generation as coal-fired power stations decline in numbers, Guicherd noted that processed landfilled ash can be a valuable source with over 1.7 billion tonnes of fly ash present in landfills.

“Air classification for improved recycling of waste dusts” by Andreas Henssen, Area Sales Manager, Neuman & Esser, focused on processing waste dusts generated by high combustion processes such as biomass combustion plants, blast furnaces and sinter plants, and cement and lime kilns.

Challenges include potential limitations for chlorides and heavy metal concentrations, and potential up-cycling of hazardous substances.

Henssen illustrated a successful example of using air classification of by-pass dust from cement manufacturing which can be recycled for use in cement and as a filler in asphalt roads.

For such applications, Neuman & Esser has developed a new classifier with an integral dispersing unit, offering optimised air flow, and sufficient dispersion to release chloride from the agglomerates for use in cement.

Steel slag

Nick Jones, Slag Technology Development Manager, Harsco Metals Group Ltd reviewed pioneering milestones in developing slag technology since 1892, and the different types of slag and their uses in “Steelmaking slag: a global resource”.

Jones noted that while across the world slag was referred to differently as waste, by-product, or product, it was nevertheless a high quality global resource. He highlighted environmental and quality challenges, and the dire consequence of material failure, such as in Ontario where a moratorium on slag use persists.

Nick Jones, Slag Technology Development Manager, Harsco Metals Group Ltd highlighted environmental and quality challenges in steel slag recycling

Applications were described in general construction, drainage, raw feed materials in cement and mineral wool, fertiliser and in road construction.

“Lixivia: Extracting value” by Mark Tilley, VP Business Development, Lixivia Inc., moved the agenda up a notch to look at recycling added value products from steel and other wastes.

“We think of industrial mineral waste as an opportunity to reconfigure existing supply chains and broaden the circular economy using chemistry” said Tilley.

In 2013, Lixivia invented a chemistry and process called SELEX to improve productivity, enable refining and develop new mineral sources that existing technology could not provide. The company is now working with partners to scale this technology. Projects include precipitated calcium carbonate (PCC), magnesia, rare earths, and lithium.

Using the SELEX process with steel slag, a proprietary hydrometallurgical process is used with a “Lixiviant” that can be recycled, which yields high purity controlled size engineered crystals of PCC with market applications in food, pharma, paper, paints and plastics.

“We think of industrial mineral waste as an opportunity to reconfigure existing supply chains and broaden the circular economy using chemistry” Mark Tilley, VP Business Development, Lixivia Inc.

Tilley concluded with some interesting cost comparisons between a typical 150,000 tpa PCC plant and a single slag recycling plant using SELEX at a steel plant site (supplying a feedstock of 400,000 tpa slag), the latter realising a slag value of $476/ton (PCC and cement ready slag additive).

In “Dry steel slag processing for high valuable products” Frank Dardemann, Technical Sales Manager, Loesche GmbH comprehensively highlighted the company’s work in stainless steel slag, LD/BOF slag, and FeCr slag, indicating further investigations on incinerator ash, non-steel slags, and concrete rubble.

Full dry processing technology has been developed for stainless steel slags with fines valorisation in standard applications such as concrete, cement, asphalt, as a reactive binder, and in alternative products, such as Carbstone. Ultrafine grinding of LD/BOF slag has enabled fines use in cement.

Aluminium salt slag

“Full recycling process for aluminium wastes, salt slags SPL treatment, and recovery” by Carlos Ruiz de Veye, Managing Director, Befesa Salt Slags Recycling, reviewed Befesa’s aluminium waste recycling process.

“In 2016, Befesa eliminated the need to dispose of 505,000 tonnes of hazardous wastes from the primary and secondary aluminium industry and reintroduced into the market a similar quantity of secondary raw materials.” said Ruiz de Veye.

“In 2016, Befesa eliminated the need to dispose of 505,000 tonnes of hazardous wastes from the primary and secondary aluminium industry and reintroduced into the market a similar quantity of secondary raw materials.” Carlos Ruiz de Veye, Managing Director, Befesa Salt Slags Recycling

In the secondary aluminium recycling loop, Befesa targets salt slags, dross fines, spent pot lining, and filter fines, which were examined by Ruiz de Veye, noting that with the closure of some aluminium smelters in Europe, less SPL may be available in the future.

Market applications include cement, ceramics, bricks, mineral wool, civil works, high alumina refractories, and steel.

Ruiz de Veye concluded with a look at development of new processes to obtain high value products such as aluminium hydroxide (ATH) for flame retardants and high purity alumina for non-metallurgical applications

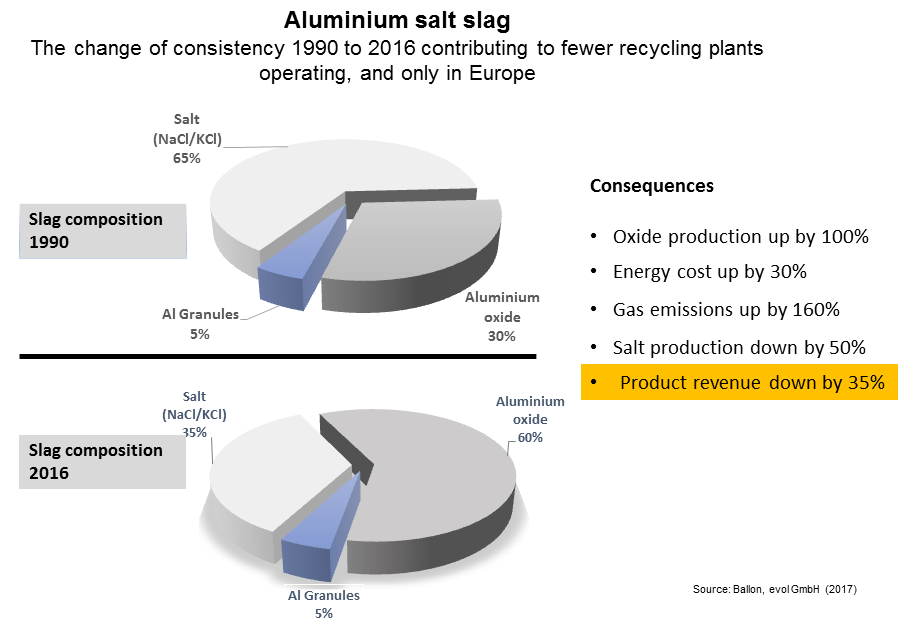

Oliver Ballon, Managing Director, evol GmbH, presented “Aluminium salt slag recycling: a reality check” by showing the entire global aluminium supply chain and check-listing the few existing plants successfully recycling aluminium waste.

Oliver Ballon, Managing Director, evol GmbH explained the main reasons why only Europe seems to be recycling Al salt slag

Ballon looked at the characterisation of Al salt slag and examined the recycling process and its products. He highlighted the main reasons for why only Europe seems to be recycling Al salt slag, which are:

• European legislation has banned landfilling of salt slag since 2000.

• The recycling process competes with landfill, which is still allowed in USA/Asia/ Middle East and Australia

• High investment for treatment plant is required

• Product revenue has dropped significantly after the technology change of secondary aluminium processors

• Sales of high alumina product are problematic

Ballon concluded with a reality check on existing potential market applications for Al salt slag products, and a look at new potential applications in steel conditioning and calcium aluminate cements.

See you next year!

As ever we are indebted to the support and participation of all of our exhibitors, speakers, and delegates for making Mineral Recycling Forum 2017 such a success.

We very much appreciate all the completed feedback forms and please continue to provide us with your thoughts and suggestions.

Sponsor & exhibit enquiries: Ismene Clarke T: +44 (0)7905 771 494 ismene@imformed.com

Presentation & programme enquiries: Mike O’Driscoll T: +44 (0)7985 986255 mike@imformed.com

We shall keep you abreast with developments for Mineral Recycling Forum 2018 and look forward to meeting you again soon.

For programme summary, feedback, attendees, and picture gallery, please go to:

Mineral Recycling Forum 2017, 7-8 March 2017, Rotterdam

Also

FREE PDF download of Mike O’Driscoll’s presentation “Recycling Industrial Minerals: a Not so Secondary Raw Material Source” given at the SME 2017 Annual Meeting, 22 February 2017, Denver

Register now for

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}